All in One TDS on Salary for Govt & Non-Govt employees for FY 2017-18 With Best Tax Saving Investments u/s 80C

Investments for Section 80C for the FY2017-18 as per Finance Budget 2017.

You can claim maximum deduction of Rs 1.5 Lakhs u/s 80C (including Sections 80CCC, 80CCD) by investing in eligible instruments. Unfortunately, investments and expenditures allowed u/s 80C is too crowded and that makes the choice difficult for most people.

Below is the list of investments/expenses eligible for deduction u/s 80C:

1. Provident Fund (EPF/ VPF)

2. Public Provident Fund (PPF)

3. Sukanya Samriddhi Account (SSA)

4. National Saving Certificate (NSC)

5. Senior Citizen’s Saving Scheme (SCSS)

6. Tax Saving Fixed Deposits (for 5 Years)

7. Life Insurance Premium

8. Pension Plans from Mutual Funds

9. Pension Plans from Insurance Companies

10. New Pension Scheme (NPS)

11. Tax Saving Mutual Funds (ELSS)

12. Central Govt. Employees Pension Scheme

13. Principal Payment on Home Loan

14. Tuition Fees for up to 2 children

15. Stamp Duty for registration of Home

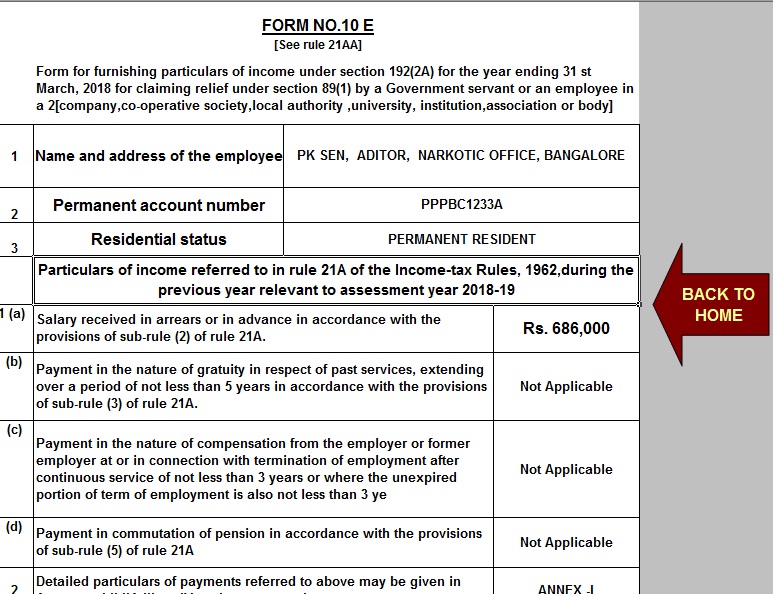

Download All in One TDS on Salary For Govt and Non-Govt employees for FY 2017-18 [This Excel utility can be prepared at a time Tax computed Sheet + Individual salary Structure + Automatic HRA Exemption + Automated Arrears Relief Calculator U/s 89(1) With Form 10E + Automated Form 16 Part B + Form 16 Part A&B for FY 2017-18]

1. Tuition Fees for up to 2 children

The expenses on tuition fees for full-time courses for the maximum of two children are eligible for deduction u/s 80C. However, the deduction is not available for tuition fee to coaching classes or private tuitions. The following expenses are not considered as tuition fees – Development Fee, Transport charges, hostel charges, Mess charges, library fees, late fines, etc.

2. Stamp Duty for registration of New Home

Stamp duty and registration charges up to Rs 1.5 Lakh can be claimed for deduction u/s 80C. The payment should have been made in the same financial year for which the tax is being paid. i.e. the deduction cannot be carried forward to next year. Also, the house should be in the name of assessee claiming the deduction.

Download Automated Arrears Relief Calculator from FY 2000-01 to FY 2017-18 as per latest Tax Slab FY 2017-18

In case you have paid stamp duty for a new home, you most probably would exhaust your 80C limit for the year and no further investment might be required.

3. Provident Funds (EPF/VPF)

EPF is a compulsory deduction for most salaried employees. The deduction can be 12% of the basic salary & dearness allowance or Rs 1,800 every month. Look at your salary statement to know how much have you contributed for the year. Count only your contribution. Employer’s contribution is not eligible for tax saving investment. You can also have some amount contributed through Voluntary Provident Fund (VPF), which can be up to 100% of the basic salary & DA.

Download HRA Exemption Calculator

3. National Pension Scheme (NPS)

NPS (Tier 1) is compulsory for most Government employees who joined after 2004. Look at your salary slip to check your deduction. Again only your contribution is a valid deduction. Employer’s contribution is not eligible. The good thing is you can use this contribution to claim an additional tax deduction up to Rs 50,000 under the newly introduced Section 80CCD(1B).

4. Home Loan Principal Amount

Are you paying the home loan? The principal component paid every year is eligible for tax deduction. For this, you can download the tax statement from banks’ website. In case not get it from the loan provider. This would give you an estimate of principal and interest paid for the financial year.

5. Insurance Premium

Have you bought life insurance products like ULIP, Endowment Plan or Term Insurance where you need to pay the premium for subsequent years? If you want to continue investing in the same you can continue to claim tax benefit.

6. PPF (Public Provident Fund)

If you have PPF account you should contribute minimum Rs 500 in a financial year. In case you don’t do, a fine is levied.

7. Sukanya Samriddhi Account (SSA)

Minimum deposit of Rs 1,000 needs to be made every year else penalty of Rs 50 is levied.

8. ELSS (Equity Linked Saving Scheme)

Popularly known as Tax saving Mutual Fund. These are equity based mutual funds and one of the best investment options to create wealth in the long run while saving tax. In case you can digest the volatility of the stock market, this is the recommended option.

9. PPF (Public Provident Fund)

PPF is another popular tax saving investment option for 80C, especially for people without any other provident fund.

10. Sukanya Samriddhi Account (SSA)

SSA can be opened by parents of girl child subject to certain conditions. SSA can be a good option for fixed income investment for a child. However, you should also invest in ELSS or other equity mutual funds for goals related to a child.

11. National Saving Certificate (NSC)

NSC can be bought at post offices to save tax u/s 80c. It is available for 5 years (NSC VIII) only. The interest offered is 8%.

12. Tax Saving Bank Fixed Deposits

India loves fixed deposits and FD which saves tax is obviously very popular.

10. NPS (National Pension Scheme)

Some of you might have to contribute compulsorily to NPS. In this case, you can take the deduction up to Rs 50,000 under the newly introduced Section 80CCD(1B). And then you can choose the more efficient investment for 80C.

No comments:

Post a Comment