Download Automated TDS on Salary All in One for Govt & Non-Govt Employees for F.Y.2018-19 including Save Tax u/s 80C For F.Y. 2018-19 Investments for Section 80C

You can claim a maximum deduction of Rs 1.5 Lakhs u/s 80C (including Sections 80CCC, 80CCD) by

investing in eligible instruments. Unfortunately, investments and

expenditures allowed u/s 80C is too crowded and that makes the choice

difficult for most people.

Below is the list of investments/expenses eligible for deduction u/s 80C:

1. Provident Fund (EPF/ VPF)

2. Public Provident Fund (PPF)

3. Sukanya Samriddhi Account (SSA)

4. National Saving Certificate (NSC)

5. Senior Citizen’s Saving Scheme (SCSS)

6. Tax Saving Fixed Deposits (for 5 Years)

7. Life Insurance Premium

8. Pension Plans from Mutual Funds

9. Pension Plans from Insurance Companies

10. New Pension Scheme (NPS)

11. Tax Saving Mutual Funds (ELSS)

12. Central Govt. Employees Pension Scheme

13. Principal Payment on Home Loan

14. Tuition Fees for up to 2 children

15. Stamp Duty for registration of Home

Download: Free e-book for Income Tax Planning for FY 2018-19

The post below suggests the approach to select the investments for tax planning.

Expenditures Eligible for Tax Benefit:

The first step is to check all expenditures which are eligible for tax deduction. Below is the list:

1. Tuition Fees for up to 2 children

The

expenses on tuition fees for full-time courses for a maximum of two

children is eligible for deduction u/s 80C. However, the deduction is

not available for tuition fee to coaching classes or private

tuitions. The following expenses are not considered as tuition fees –

Development Fee, Transport charges, hostel charges, Mess charges,

library fees, Late fines, etc.

2. Stamp Duty for registration of New Home

Stamp

duty and registration charges up to Rs 1.5 Lakh can be claimed for

deduction u/s 80C. The payment should have been made in the same

financial year for which the tax is being paid. i.e. the deduction

cannot be carried forward to next year. Also, the house should be in the

name of assessee claiming the deduction.

In

case you have paid stamp duty for a new home, you most probably would

exhaust your 80C limit for the year and no further investment might be

required.

Compulsory Deductions:

There

are some compulsory deductions that are eligible for tax benefit u/s

80C. Check if you contribute in any of such deductions:

1. Provident Funds (EPF/VPF)

EPF is

a compulsory deduction for most salaried employees. The deduction can

be 12% of the basic salary & dearness allowance or Rs 1,800 every

month. Look at your salary statement to know how much have you

contributed for the year. Count only your contribution. Employer’s

contribution is not eligible for tax saving investment. You can also

have some amount contributed through Voluntary Provident Fund (VPF), which can be up to 100% of the basic salary & DA.

2. National Pension Scheme (NPS)

NPS (Tier 1) is

compulsory for most Government employees who joined after 2004. Look at

your salary slip to check your deduction. Again only your contribution

is a valid deduction. Employer’s contribution is not eligible. The

good thing is you can use this contribution to claim an additional tax

deduction up to Rs 50,000 under the newly introduced Section 80CCD(1B). We have explained this in the last paragraph of the post.

Recurring Deductions:

There are some deductions which happen year on year like home loan repayment, insurance premium etc.

1. Home Loan Principal Amount

Are

you paying the home loan? The principal component paid every year is

eligible as a tax deduction. For this, you can download the tax

statement from the banks’ website. In case not get it from the loan

provider. This would give you an estimate of principal and interest paid

for the financial year.

2. Insurance Premium

Have

you bought life insurance products like ULIP, Endowment Plan or Term

Insurance where you need to pay the premium for subsequent years? If you

want to continue investing in the same you can continue to claim tax

benefit.

3. PPF (Public Provident Fund)

If you have PPF account you should contribute minimum Rs 500 in a financial year. In case you don’t do, a fine is levied.

4. Sukanya Samriddhi Account (SSA)

Minimum deposit of Rs 1,000 needs to be made every year else penalty of Rs 50 is levied.

5. NPS

Do you have NPS account? A minimum contribution of Rs 1,000 is required every financial year to keep the account active.

For

many people, the 80C deduction limit is reached by this time. In case

not, choose from the list below depending on your risk profile and

investment goals:

New Investment for 80C:

1. Term Life Insurance

Do

you have dependents? Would they survive financially in case something

happens to you? Do you have enough life insurance? If no go get a term

insurance first. It’s important to opt for protection first.

Useful Tips:

§ Online term plans are much cheaper than offline. So it makes sense to go for online plans.

§ Do not provide false information in the insurance form. The insurance claim can be rejected for wrong information.

§ Do not buy anything other than Term Plans from insurance companies. No money back, endowment plans!

2. ELSS (Equity Linked Saving Scheme)

Popularly known as Tax saving Mutual Fund. These are equity-based mutual funds and one of the best investment options to create wealth in the long run while saving tax. In case you can digest the volatility of the stock market, this is the recommended option.

Lock-in Period: 3 Years

The Good:

§ Among the tax saving investments, ELSS has least lock-in period of 3 years.

§ The gains on ELSS Fund is Tax-Free.

§ Convenient to buy and manage as ELSS can be bought and redeemed online.

The Bad:

§ There can be considerable volatility in returns and you can get negative returns at the end of 3 years.

Helpful Tips:

§ Invest through SIP (Systematic Investment Plan). This helps in tiding over volatility to some extent.

§ Choose “Growth” option over “Dividend Payout” as this creates wealth in the long run.

§ Try

to invest directly to fund as this would give you 0.5% to 1% higher

returns as compared to when you invest through a broker If doing

lump-sum check for stock market valuations. If you invest at high

valuations, you might see very low or negative returns at the end of 3

years.

§ Avoid “closed-ended” ELSS NFOs which are launched at this time of the year.

3. PPF (Public Provident Fund)

PPF is another popular tax saving investment option for 80C, especially for people without any other provident fund.

Lock-in Period: 15 Years. However partial withdrawal is allowed from 7th year

The Good:

§ The interest earned on PPF is Tax-Free

§ After opening the PPF account, investment can be done online every Year (for some banks)

§ Highest Safety – backed by Govt. of India

The Bad:

§ The lock-in is for 15 years but there is partial liquidity from 7th year onwards.

Helpful Tips:

§ Investment done till 5th of the month earns interest for the month. So deposit your money before 5th of a month

§ You

can use a combination of PPF and ELSS for tax saving investments. In

case you find stock market over-valued, PPF is a good option.

4. Senior Citizen’s Saving Scheme (SCSS)

SCSS

is a good option for senior citizens (above 60 years of age) as it

gives regular quarterly interest income directly in a bank account.

Lock-in: 5 years

§ Highest Safety – backed by Govt. of India

§ The interest rate offered is highest among the small saving schemes

The Bad:

§ The interest received is taxable.

§ TDS

would be deducted if the total interest in a year is over Rs 10,000.

However, if eligible Form 15H can be submitted to avoid TDS.

Helpful Tips:

§ SCSS account can be closed after 1 Year (with penalty) but in case you have availed Sec 80C benefit, it would be reversed.

§ The joint account can be opened only with your spouse. There is no age limit applicable for the joint account holder.

5. Sukanya Samriddhi Account (SSA)

SSA

can be opened by parents of girl child subject to certain conditions.

SSA can be a good option for fixed income investment for the child.

However, you should also invest in ELSS or other equity mutual funds for

goals related to the child.

Lock-in: Deposit to the account to be made for 14 years and account matures at 21 years from the date of opening

The Good:

§ The interest earned on SSA is Tax-Free and also higher than that offered to PPF

§ 50% withdrawal allowed when a girl turns 18 for marriage/higher education

§ Highest Safety – backed by Govt. of India

The Bad:

§ No provision of Loan or pre-mature withdrawal unlike PPF

Helpful Tips:

§ Minimum deposit of Rs 1,000 needs to be made every year else penalty of Rs 50 is levied

§ Account can be closed before 21 years in case of marriage

6. National Saving Certificate (NSC)

NSC

can be bought at post offices to save tax u/s 80c. It is available for 5

years (NSC VIII) only. The interest offered is 7.8%.

Lock-in: 5 Years

The Good:

§ The interest is higher than most tax saving bank fixed deposits.

§ Certificates can be kept as collateral security to get a loan from banks

§ No Tax deduction at source

§ The interest accrued for NSC qualifies for Sec 80C deduction in subsequent years

§ Highest Safety – backed by Govt. of India

The Bad:

§ The interest earned is taxable

§ You

need to visit the Post office for buying and redeeming NSC units. This

can be a hassle for people who shift addresses frequently.

Also Read: Calculate Tax on Arrears in 7 Easy Steps

Helpful Tips:

§ You can buy NSC in denominations of Rs 100, 500, 1000, 5000 and 10000

§ NSC

is better to tax saving option than banks Tax Saving FD (offering

similar interest) as interest accrued for NSC qualifies for Sec 80C

deduction in subsequent years

7. Tax Saving Bank Fixed Deposits

Also Read: Highest Tax Saving Bank Fixed Deposit Rates U/S 80C across 44 banks

Lock-in: 5 years

The Good:

§ Convenient to invest. Many banks offer online facility for Tax Saving FD

§ High Safety – FD up to Rs 1 Lakh is insured by RBI

The Bad:

§ The interest received is taxable. (Tax treatment of Fixed Deposits)

§ Cannot be withdrawn prematurely

§ Cannot be pledged to secure a loan or as security

Helpful Tips:

§ The minimum tenure is of 5 Years. Some banks offer special schemes for longer tenures with slightly higher interest rates

§ Don’t be mislead by banks advertisements about their yield on Tax Saving FDs. Those are manipulative calculations. [SBI Tax Saving Deposit Scheme – Interest & Annual Yield]

§ Be cautious of small co-operative banks as they have a higher risk than bigger private and public sector banks.

8. Pension Plans from Mutual Funds

There are Pension plans from mutual funds which offer tax benefit u/s 80C:

1. Templeton India

2. UTI Retirement Benefit Pension Fund

3. Reliance Mutual Fund Pension Plan

The

above funds are hybrid or balanced mutual funds – the first two funds

are debt oriented mutual fund while the one from Reliance has two funds –

one debt oriented and other equity-oriented.

Lock-in: 5 years

Helpful Tips:

§ Reliance

Mutual Fund Pension Plan is a better option among the three funds as

you use Wealth option (which is equity oriented fund) to create the

corpus and then switch to Income option (which is debt oriented fund)

for regular income after retirement.

§ All 3 funds levy exit load to discourage people from exiting early

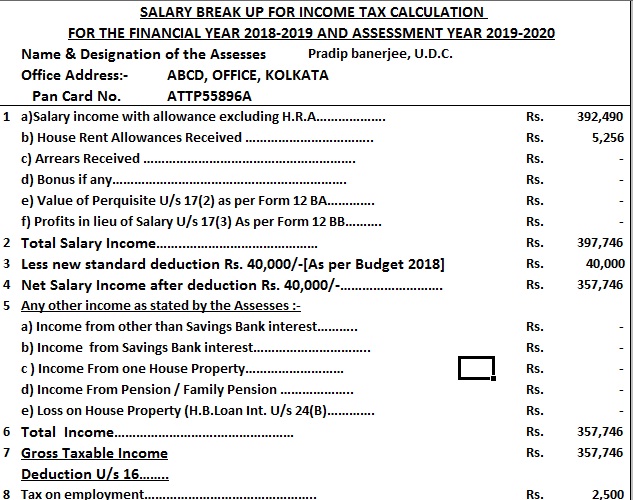

Download: Excel-based Income Tax Calculator for Non-Govt Employees All in One TDS on Salary for FY 2018-19[AY 2019-20 [ This Excel utility can prepare at a time your Income Tax Computed Sheet + Individual Salary Sheet + Individual Salary Structure + Automatic H.R.A. Calculation + Automated Income Tax Form 16 Part A&B and Form 16 Part B for F.Y. 2018-19 ]

9. NPS (National Pension Scheme)

Some

of you might have to contribute compulsorily to NPS. In this case, you

can take a deduction up to Rs 50,000 under the newly introduced Section

80CCD(1B). And then you can choose a more efficient investment in 80C.

No comments:

Post a Comment