We all have Bank Fixed Deposit (FD), at least a one. However, have you ever thought of what will happen when depositor dies before maturity? Whether your nominees or family members know the rules?

Recently, one of my blog readers asked this question. His father had some Bank Fixed Deposit (FD). Recently, his father died. Therefore, this reader is in a dilemma of whether to inform the bank now itself and withdraw the money or he has to wait till maturity. Remember, this particular Bank Fixed Deposit (FD) was fixed at a higher interest rate than what it is available now.

Before understanding this common problem. First, let us understand the rights of a nominee in case of Bank Fixed Deposit (FD). It is very much important to appoint nominee in all your financial transactions. In the case of Bank Fixed Deposit (FD), below are the few rights of nominees.

- Nominee acts like trust. He has no rights over the asset. He simply acts as a custodian and makes sure that the deposit must reach to a proper legal heir. However, he can claim the amount only when it is specified under the will or if he inherits the money.

- He is the contact person in case the depositor dies before maturity.

- He has to submit the proof while claiming the amount.

- The nominee must be an individual and one member. HUF, trust or societies can’t appoint nominees.

- If you haven’t appointed nominee during creating Bank Fixed Deposit (FD), you can do so at a later stage too (but before maturity).

In how many ways, we can hold the Bank Fixed Deposit (FD)?

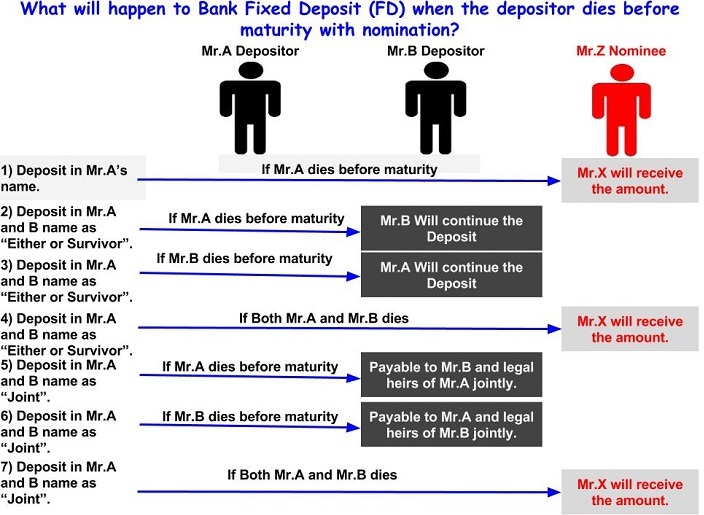

- Joint holding with “Anyone or Survivor” option-This is the best way to deposit. Because, in a case of death of a first holder or joint holder, the survivor may claim the deposit easily. The survivor has to produce the death certificate to the bank. Upon receipt of the same, banks will delete the deceased person’s name and the FD will turn to be in the name of a survivor. In such a situation, the FD is continued as usual and not considered as a death of a depositor.

- Joint holding with “Joint Holding” option-In such types of Bank Fixed Deposit (FD), the holding will be joint. All joint holder’s signature is a must to claim the deposit at maturity. In the event of a death of anyone holder, the surviving holder may claim the rights over deposit by producing the proper documents. In a case of death of both holders, then the money will be payable to a nominee.

- Single holding with “Nomination” option-If depositor dies before maturity, then the maturity proceeds will be payable to a nominee (as a custodian or trust). At a later stage, the amount will be fixed based on the WILL or Succession Certificate.

- Single holding without “Nomination” option-If there is no nomination, then the family members must produce the legal heir proof or a succession certificate to claim the amount. This is the most lengthy process.

The same scenarios are explained in below image when the depositor nominated someone.

Now what will happen if the depositor not nominated? The process will be difficult to claim for the survivors. The same is explained in below image.

Note-For simplification purpose, I created Mr.Z as legal heir of both Mr.A and Mr.B. However, in reality you may find different. In case of deposit without a nomination, the maturity will be payable to the legal heirs of deceased or any one of them mandated by all the legal heirs.

Documents required to claim the Bank Fixed Deposit (FD) of the deceased person (when the nomination is there)

- Claim Form-This is nothing but a letter to Bank stating that the depositor died and you are being a nominee, claiming the deposit. The format will be available with the Bank.

- Death Certificate-You have to produce the death certificate issued by local authorities.

- Proof of Address and Photo ID-You have to produce the address proof and photo identity of the nominee or the survivor.

Documents required to claim the Bank Fixed Deposit (FD) of the deceased person (when the nomination is not there)

- Succession Certificate from Legal Heirs-You have to produce the succession certificate.

- Indemnity Bond (format will be available with banks).

Whether to continue or withdraw the deposit?

After the death of a depositor, the nominee has two options. One is to continue the FD till maturity. Second is to withdraw it immediately. In the case of withdrawal, banks will not charge any penalty.

You can act according to the current interest rate cycle and the deposit interest rate. Suppose the FD interest rate is around 10% and currently the same bank offering FD at 8%, then it is better to continue the FD till maturity. If there is a reverse situation, then you can withdraw it.

How you receive the maturity amount?

Here RBI had provided two options and are as below.

“a) The bank could be authorized by the survivor(s) / nominee of a deceased account holder to open an account styled as ‘Estate of Shri ________________, the Deceased’ where all the pipeline flows in the name of the deceased account holder could be allowed to be credited, provided no withdrawals are made.OR

- b) The bank could be authorized by the survivor(s) / nominee to return the pipeline flows to the remitter with the remark ‘Account holder deceased’ and to intimate the survivor(s) / nominee accordingly. The survivor(s) / nominee / legal heir(s) could then approach the remitter to effect payment through a negotiable instrument or through ECS transfer in the name of the appropriate beneficiary.“

You are notice that claiming deposit when there is no nomination is a hardship. Hence, to avoid this situation, always create FDs with a nomination. Hope this information will be helpful to all.