Modified Income deduction Under Chapter VIA & 80C as per new Finance Budget 2014

HRA exemption = Least of (40% (50% for metros) of Basic+DA or HRA or rent paid - 10% of Basic+DA)

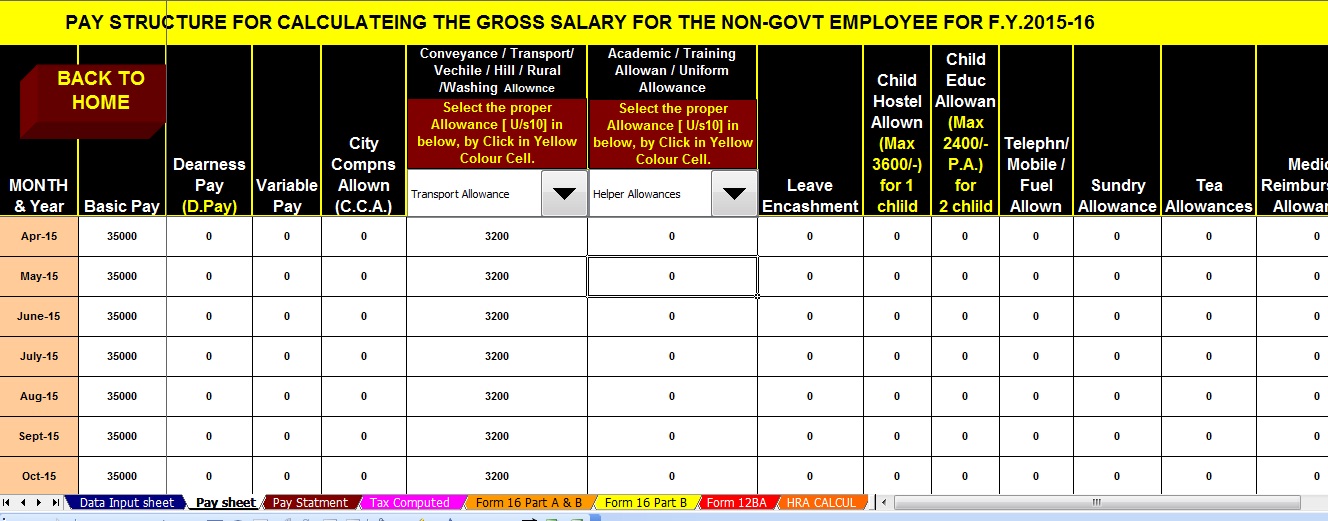

Transport allowance is exempt up to Rs.800/- per month during the month. (Expenditure incurred for covering journey between office and residence.) For people having permanent physical disability, the exemption is 1,600/- per month.

Reimbursement of Medical bills are exempt for self and dependent family, up to Rs.15,000/- per annum u/s(5) LTA is exempt to the tune of economy class Train/ Air /Recognised public Transport fare for the family to any destination in India, by the shortest route.

LTA can be claimed twice in a block of 4 calendar years. The current block is from 01.01.2010 to 31.12.2013. For claim, it is must to provide originals tickets etc.

U/s 24 There is an Exemption for interest on housing loan. Exemption is limited to Rs. 2,00,000/- per year if the house is self-occupied; There is no limit if the house is rented out.

U/s 80C- Maximum Exemption up to Rs. 150000/- Investments up to Rs. 1.5 lac in PF, VPF, PPF, Employee contribution in NPS,Insurance Premium, Housing loan principal repayment, NSC, ELSS, long term bank Fixed Deposit, Post Office Term Deposit, etc. are deductible from the taxable income. Item wise 80C deduction is given below as per the latest amended by the Finance Budget 2014.

- Provident Fund (PF) & Voluntary Provident Fund (VPF) PF is automatically deducted from your salary. your contribution [12% of Basic] (i.e., employee’s contribution) is counted towards section 80C investments. You also have the option to contribute additional amounts through voluntary contributions (VPF). Current rate of interest is 8.5% per annum (p.a.) and is tax-free.

- Life Insurance Premiums: Any amount that you pay towards life insurance premium in Life Insurance Corporation (LIC) or any other Insurance CO.for yourself, your spouse or your children can also be included in Section 80C deduction. If you are paying premium for more than one insurance policy, all the premiums will be included. also premium paid for ULIP will also be treated as Premium paid for Life Insurance Policies.

- Unit linked Insurance Plan : ULIP stands for Unit linked Saving Schemes. ULIPs cover Life insurance with benefits of equity investments.They have attracted the attention of investors and tax-savers not only because they help us save tax but they also perform well to give decent returns in the long-term.

- Public Provident Fund (PPF) is one of the best. Current rate of interest is 8% tax-free and the normal maturity period is 15 years. Minimum amount of contribution is Rs. 500 and maximum is Rs. 1,50,000.(New Change) from Budget 2014

- National Savings Certificate (NSC): National Savings Certificate (NSC) is a 5-Yr small savings instrument eligible for section 80C tax benefit. Rate of interest is 8.58% compounded half-yearly, i.e. If you invest Rs.100, it becomes Rs.150.90 after five years. The interest accrued every year is liable to tax (i.e. to be included in your taxable income) but the interest is also deemed to be reinvested and thus eligible for section 80C deduction.

- Home Loan Principal Repayment & Stamp Duty and Registration Charges for a home Loan The Equated Monthly Installment (EMI) that you pay every month to repay your home loan consists of two components – Principal and Interest.The principal component of the EMI qualifies for deduction under Sec 80C. Even the interest component can save you significant income tax – but that would be under Section 24 of the Income Tax Act. The amount you pay as stamp duty when you buy a house, and the amount you pay for the registration of the documents of the house can be claimed as deduction under section 80C in the year of purchase of the house.

- Tuition fees for 2 children Apart form the above major investments expenses for children’s education (Only Tution Fee (for which you need receipts)), can be claimed as deductions under Sec 80C.

- Equity Linked Savings Scheme (ELSS): There are some mutual fund (MF) schemes specially created for offering you tax savings, and these are called Equity Linked Savings Scheme, or ELSS. The investments that you make in ELSS are eligible for deduction under Sec 80C.

- 5-Yr bank fixed deposits (FDs): Tax-saving fixed deposits (FDs) of scheduled banks with tenure of 5 years are also entitled for section 80C deduction.

- 5-Yr post office time deposit (POTD) scheme: POTDs are similar to bank fixed deposits. Although available for varying time duration like one year, two year, three year and five year, only 5-Yr post-office time deposit (POTD) – which currently offers 7.5 per cent rate of interest –qualifies for tax saving under section 80C. Effective rate works out to be 7.71% per annum (p.a.) as the rate of interest is compounded quarterly but paid annually. The Interest is entirely taxable.

- Pension Funds or Pension Policies – Section 80CCC: This section – Sec 80CCC – stipulates that an investment in pension funds is eligible for deduction from your income. Section 80CCC investment limit is clubbed with the limit of Section 80C – it means that the total deduction available for 80CCC and 80C is Rs 1.5 Lakh.This also means that your investment in pension funds upto Rs.1.5 Lakh can be claimed as deduction u/s 80CCC. However, as mentioned earlier, the total deduction u/s 80C and 80CCC can not exceed Rs.1.5 Lakh.

- Infrastructure Bonds: These are also popularly called Infra Bonds. These are issued by infrastructure companies, and not the government. The amount that you invest in these bonds can also be included in Sec 80C deductions.

- NABARD rural bonds: There are two types of Bonds issued by NABARD (National Bank for Agriculture and Rural Development): NABARD Rural Bonds and Bhavishya Nirman Bonds (BNB). Out of these two, only NABARD Rural Bonds qualify under section 80C.

- Senior Citizen Savings Scheme 2004 (SCSS): A recent addition to section 80C list, Senior Citizen Savings Scheme (SCSS) is the most lucrative scheme among all the small savings schemes but is meant only for senior citizens. Current rate of interest is 9% per annum payable quarterly. Please note that the interest is payable quarterly instead of compounded quarterly. Thus, unclaimed interest on these deposits won’t earn any further interest. Interest income is chargeable to tax.

U/s 80CCD -The Finance Act, 2011 provides that contribution made by the Central Government or any other employer to NPS (up to 10 per cent of the salary of the employee in the previous year)shall be excluded while computing the limit of Rs. 1,50,000.The contribution by the employee to the NPS will be subject to the limit of Rs. 1,00,000.

U/s 80CCG - Rajiv Gandhi Equity Savings Scheme is a new exemption available for investment in stock markets (direct equity). Avaialble only for those with gross income less than 12 lacs and only for first time investors in stock market. Exemption available at 50% of investment subject to maximum of Rs.50,000/- invested. Investments are locked-in for three years

U/s 80D Medical Insurance Premium (such as Mediclaim & Critical illness Cover)& Health Check up Upto Rs. 5000, premium is exempt up to Rs. 30,000/ per year (Rs.15,000/- for self,spouse and children ) (Rs. 15000/- for Parents. If the premium includes for a dependent who is (Senior Citizen) above 60 years of age, an extra Rs. 5,000//- can be claimed.

U/s 80DD Deduction in respect of medical treatment of handicapped dependents is limited to Rs. 50,000/- per year if the disability is less than 80% and Rs. 1,00,000/- per year if the disability is more than 80%

U/s 80DDB Deduction in respect of medical treatment for specified ailments or diseases for the assesse or dependent can be claimed up to Rs. 40,000/- per year. If the person being treated is a senior citizen, the exemption can go up to Rs. 60,000/-. but any amount received under Medical Insurance Policy will be reduced from the amount of deduction allowed. The Diseases and ailments specified under rule 11DD are.

- neurological diseases being demetia, dystonia musculorum deformans, motor neuron disease, ataxia, chorea, hemiballismus, aphasia and parkisons disease,

- cancer,

- AIDS,

- Chronic renal failure,

- hemophilia, and

- thalassaemia.

U/s 80E Interest repayment on education loan (taken for higher education from a university of self & dependents) is completely tax exempt

U/s 80G Donations given for certain charities are tax exempt. Some(NGO,Trust etc.) are exempt to the tune of 50%, whereas Govt funds are 100%.

U/s 80GG If you are not getting HRA, but living in rented house, an exemption is available. This will be calculated as minimum of (25% of total income or rent paid - 10% of total income or Rs. 24,000/- per year)

U/s 80U who suffers from not less than 40 per cent of any disability is eligible for deduction to the extent of Rs. 50,000/- and in case of severe disability to the extent of Rs. 100,000/-

U/s 80TTA introduced through Finance Act, 2012. Section 80TTA provides a deduction of up to Rs. 10,000 on your income from interest on saving bank accounts.

U/s 87A Tax Rebate Rs.2,000/- who's taxable income less than 5 Lakh.