The Income Tax Section Under Section 80GG where allow the House Rent Exemption Maximum Rs. 60,000/- P.A. OR 5000/- P.M. who have not get the House Rent allowances from the employer. The Section 80GG says in brief is given below:-

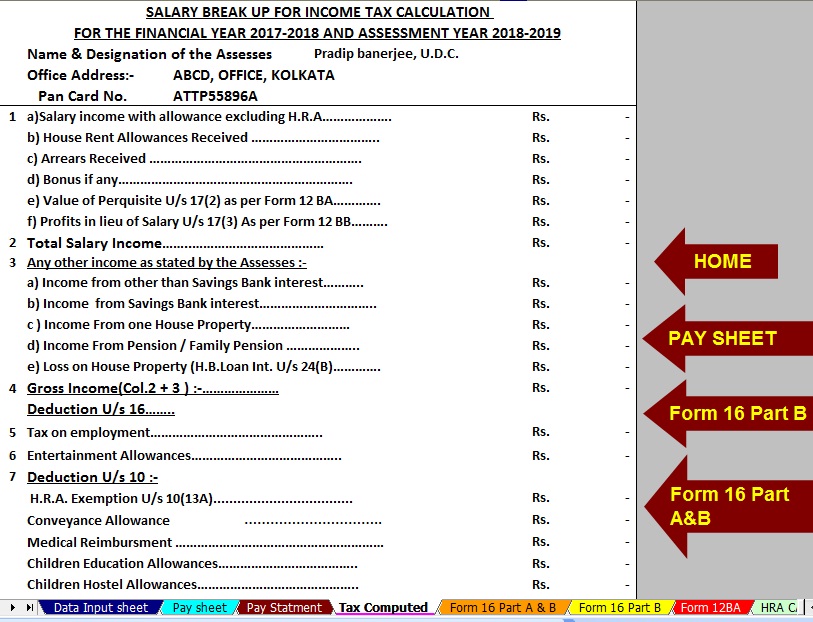

Download Private employees Income Tax Preparation Excel Based Software For F.Y2017-18 & A.Y. 2018-19 [This Utility can prepare at a time your Income Tax Calculated Sheet + Individual Salary Structure as per the any Private Employees Salary Structure / Non Govt Concerned for calculate the Gross Salary Amount + Automatic House Rent Exemption Calculation + Form 12 BA + Automated Form 16 Part B and Part A&B for the Financial Year 2017-18 and Assessment Year 2018-19 this Excel Utility only for Private Employees. This Excel Utility prepare as per the Finance Budget 2017-18 with all amended Income Tax Section with New Tax Slab for F.Y.2017-18]

Feature of above utility:-

- Automatic Calculate the Income Tax Liability

- Inbuilt Salary Structure for Private Concerned as per Private employees Salary Structure

- Easily Calculate your Gross Salary Income by the Salary Structure

- Automatic HRA Calculation

- Automated Form 16 Part B and Form 16 Part A&B

- This Excel Utility only for Private or Non Govt Employees

Details of Income Tax Section 80GG :-

Section 80GG allows the employee to a deduction in respect of house rent paid by him for his own residence. Such deduction is permissible subject to the following conditions:-

(a) The employee has not been in receipt of any House Rent Allowance

specifically granted to him which qualifies for exemption under section 10(13A) of the Act;

(b) The employee files the declaration in Form No.10BA. (Annexure X)

(c) The employee does not own:

(i) any residential accommodation himself or by his spouse or minor child or where such employee is a member of a Hindu Undivided Family, by such family, at the place where he ordinarily resides or performs duties of his office or carries on his business or profession; or

(ii) at any other place, any residential accommodation which is in the occupation of the employee, the value of which is to be determined under section 23(2)(a) or section 23(4)(a), as the case may be.

(d) He will be entitled to a deduction in respect of house rent paid by him in excess of 10% of his total income. The deduction shall be equal to 25% of total income or Rs. 5,000/- per month, whichever is less. The total income for working out these percentages will be computed before making any deduction under section 80GG.

The Drawing and Disbursing Authorities should satisfy themselves that all the conditions mentioned above are satisfied before such deduction is allowed by them to the employee. They should also satisfy themselves in this regard by insisting on production of evidence of actual payment of rent.