The Income Tax Section Under Section 80GG where allow the House Rent Exemption Maximum Rs. 60,000/- P.A. and 5000/- P.M. who have not get the House Rent allowances from the employer. The Section 80GG says, in brief, is given below:-

Showing posts with label HRA Calculator. Show all posts

Showing posts with label HRA Calculator. Show all posts

Sunday, 11 March 2018

Sunday, 4 March 2018

Monday, 1 May 2017

The Income Tax Section Under Section 80GG where allow the House Rent Exemption Maximum Rs. 60,000/- P.A. OR 5000/- P.M. who have not get the House Rent allowances from the employer. The Section 80GG says in brief is given below:-

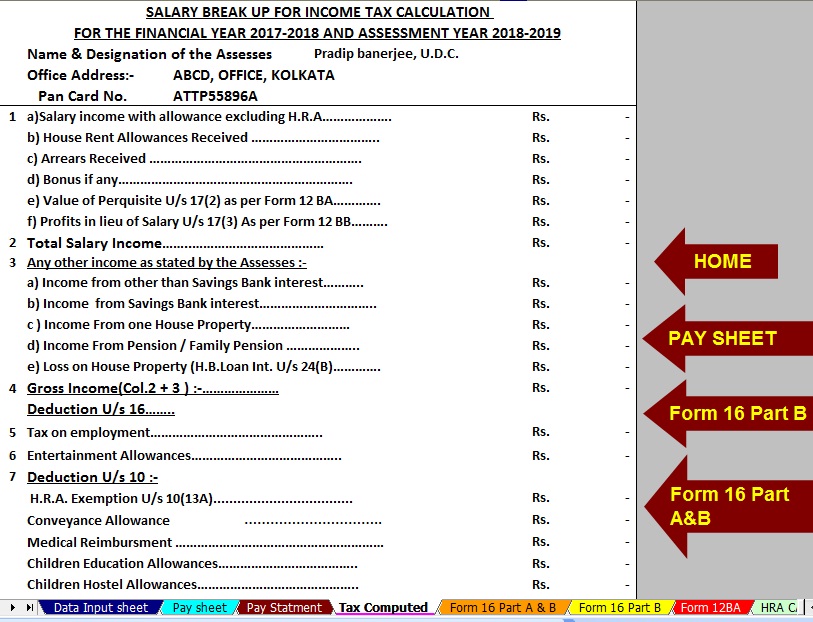

Download Private employees Income Tax Preparation Excel Based Software For F.Y2017-18 & A.Y. 2018-19 [This Utility can prepare at a time your Income Tax Calculated Sheet + Individual Salary Structure as per the any Private Employees Salary Structure / Non Govt Concerned for calculate the Gross Salary Amount + Automatic House Rent Exemption Calculation + Form 12 BA + Automated Form 16 Part B and Part A&B for the Financial Year 2017-18 and Assessment Year 2018-19 this Excel Utility only for Private Employees. This Excel Utility prepare as per the Finance Budget 2017-18 with all amended Income Tax Section with New Tax Slab for F.Y.2017-18]

Feature of above utility:-

- Automatic Calculate the Income Tax Liability

- Inbuilt Salary Structure for Private Concerned as per Private employees Salary Structure

- Easily Calculate your Gross Salary Income by the Salary Structure

- Automatic HRA Calculation

- Automated Form 16 Part B and Form 16 Part A&B

- This Excel Utility only for Private or Non Govt Employees

Details of Income Tax Section 80GG :-

Section 80GG allows the employee to a deduction in respect of house rent paid by him for his own residence. Such deduction is permissible subject to the following conditions:-

(a) The employee has not been in receipt of any House Rent Allowance

specifically granted to him which qualifies for exemption under section 10(13A) of the Act;

(b) The employee files the declaration in Form No.10BA. (Annexure X)

(c) The employee does not own:

(i) any residential accommodation himself or by his spouse or minor child or where such employee is a member of a Hindu Undivided Family, by such family, at the place where he ordinarily resides or performs duties of his office or carries on his business or profession; or

(ii) at any other place, any residential accommodation which is in the occupation of the employee, the value of which is to be determined under section 23(2)(a) or section 23(4)(a), as the case may be.

(d) He will be entitled to a deduction in respect of house rent paid by him in excess of 10% of his total income. The deduction shall be equal to 25% of total income or Rs. 5,000/- per month, whichever is less. The total income for working out these percentages will be computed before making any deduction under section 80GG.

The Drawing and Disbursing Authorities should satisfy themselves that all the conditions mentioned above are satisfied before such deduction is allowed by them to the employee. They should also satisfy themselves in this regard by insisting on production of evidence of actual payment of rent.

Sunday, 16 October 2016

All in One Income Tax preparation Excel Based Software for West Bengal Govt employees For F.Y. 206-07 ( This Excel Utility can prepare at a time your Tax Compute Sheet + Individual Salary Structure + Individual Salary Sheet + Automated HRA Calculation + Form 16 Part A&B and Part B)

The Financial Year have already started since the 1/4/2016 and which will be the end of March 2017. In this Financial year have already passed the New Central Finance Bill and some Income Tax Section introduce to the Income Tax Payers ( All Salaried Persons). It is observed that the Income Tax Slab has changed up to Rs. 2.5 Lakh and the Section 80C also Raised up to Rs. 1.5 Lakh in this Financial Year 2016-17, Tax Slab For Men and Women is Rs. 2,50,000/- = NIL and 2,00,001 to 10,00,000/- Tax @ 10% and above 10,00,000/- @30%.

The New Income Tax Section started from the Financial Year 2013-14 is given below:-

Section 87A Tax Rebate Rs. 5,000/- who's Taxable Income not more than 5,00,000/-

Section 80EE, House Building Loan Interest who's HBL interest started since 1/4/2013 Max Rs. 1,50,000/- additional amount of U/s 24 B.

Thursday, 7 January 2016

Download the Automated All in One TDS on Salary for All State Govt Employees for Financial Year 2015-16

[ This Excel Based Software can prepare at a time your Tax Compute

Sheet + Individual Salary Structure + Individual Salary Sheet +

Automatic HRA Calculation U/s 10(13A) +Automatic Form 16 Part A& B

and Automatic Form 16 Part B as per the new Finance Budget 2015]

|

| Deductor & Employee Details |

Employee Salary Structure

|

| Employee Tax Computed Sheet |

|

| Form 16 Part A&B |

|

| Employees Individual Salary Sheet |

No

changes in tax slab rate for the F.Y.2015-16. The tax free income remains 2.5

lakh. There is some concession in medical insurance. But 80C limit of Rs 1.5

lakh will remain for another one year. Rather income tax surcharge is

increased. However, investment in New Pension Scheme will give you extra

tax saving.

- You can get extra tax deduction up to Rs 50,000 by investing in New Pension Scheme U/s 80CC i.e. Total Deduction can get Rs. 1.5 Lakh

- The tax deduction limit for health insurance is also increased 25,000/- for below 60 years of age and For the senior citizen this limit is now Rs 30,000/-.

- Senior citizens who are older than 80 years and don’t have any health insurance, can claim tax deduction on medical expense of Rs 30,000.

- From the financial year 2015-16 the the riches would have to pay more tax as surcharge is increased to 12%. Earlier it was 10%. Surcharge is levied upon those who earn more than Rs one crore in a year.

- Transport Allowance exemption limit is increased to 1,600/month. & For Phy.disable Person can get Rs.3200/- Per month

Monday, 6 July 2015

The

Central Finance Budget 2015 has made following changes relating to

determination of Income Tax payable by Salaried Employees, which provide

income tax exemption.

1.

Taxable Income eligible for full exemption from income tax Rs. 2.5 lakh

same as previous Financial Year, there have no any changed.

2. Tax Rebate Rs. 2,000/- U/s 87A is entitled in this Financial Year 2015-16 as well it will be continued this Financial Year.

3. Include Addition Deduction U/s 80C as Sukanya Samriddhi Account , Max Rs.1.5 Lakh

2. Tax Rebate Rs. 2,000/- U/s 87A is entitled in this Financial Year 2015-16 as well it will be continued this Financial Year.

3. Include Addition Deduction U/s 80C as Sukanya Samriddhi Account , Max Rs.1.5 Lakh

Click to Download Central Govt employees All in One TDS on Salary with automated Form 16 for FY 2015-16 (Ass Year 2016-17)[ This Excel utility can prepare at a time Tax Compute sheet + Individual Salary Sheet + Automatic HRA Calculation + Automated Form 16 Part A&B and Part B for FY 205-16]

Snapshot of Salary Structure of Central Govt Employees

Click to Download all State Govt employees All in One TDS on Salary with automated Form 16 for FY 2015-16 (Ass Year 2016-17)[This Excel Based Utility can prepare at a time your Tax Compute Sheet + Individual Salary Sheet +Automatic HRA Exemption Calculation + Automatic Form 16 Part A&B and Part B for FY 2015-16]

Snapshot of Salary Structure of State Govt Employees

The Main Changes in income tax exemptions applicable for the year 2015-16 is as follows:-

Transport Allowance:

Transport

Allowance granted to an employee to meet expenditure for the purpose of

commuting between the place of residence and place of duty. Income Tax

Exemption on Transport Allowance is Raised Rs1600/- per month for

general and Rs.3200/- P.M. for Phi. Disable persons.

Section 80C:

The total deduction under

this section (along with section 80CCC and 80CCD) is limited to Rs.

1.50 lakh. Some investments, savings, expenditure etc covered under

Section 80 C

Section 80CCD (1): Deduction in respect of Contribution to Pension Account (by Assessee)

Deduction available for the amount paid or deposited in a pension scheme notified or as may be notified by the Central Government subject to a maximum of :

(a) 10% of salary in the previous year in the case of an employee (b) 10% of gross total income in any other case.

Section 80CCD (2): Deduction in respect of Contribution to Pension Account (by Employer)

Deduction available for the amount paid or deposited by

the employer of the assessee in a pension scheme notified or as may be

notified by the Central Government subject to a maximum of 10% of salary

in the financial year. This exemption is in addition to Rs. 1.5 lakh

limit provided under Section 80 CCE for deductions under Section 80 C,

CCC, and 80CCD(1)

Deductions under Chapter VIA of Income Tax Act [ Click here to view all deduction under Chapter VIA updated]

Section 80CCG: Rajiv Gandhi Equity Saving Scheme (RGESS)

As

per the Budget 2012 announcements, a new scheme Rajiv Gandhi Equity

Saving Scheme (RGESS) will be launched. Those investors whose annual

income is less than Rs. 10 lakh (proposed Rs. 12 lakh from A.Y. 2014-15)

can invest in this scheme up to Rs. 50,000 and get adeduction of 50% of the investment. So if you invest Rs. 50,000 (maximum amount eligible forincome tax rebate is Rs. 50,000), you can claim a tax deduction of Rs. 25,000 (50% of Rs. 50,000).

Section 80D: Deduction in respect of Medical Insurance

Deduction is

available up to Rs. 30,000/- for senior citizens and up to Rs. 25,000/

in other cases for insurance of self, spouse and dependent children.

Additionally, a deduction for

insurance of parents (father or mother or both) is available to the

extent of Rs. 30,000/- if parents are senior Citizen and Rs. 25,000/- in

other cases. Therefore, the maximum deduction available under this section is to the extent of Rs. 55,000/-. From AY 2016-17.

Section 80DDB: Deduction in respect of Medical Expenditure on Self or Dependent Relative

A deduction to the extent of Rs. 80,000/- or the amount actually paid, whichever is less is available for expenditure actually incurred

by resident assessee on himself or dependent relative for medical

treatment of specified disease or ailment. The diseases have been

specified in Rule 11DD. A certificate in form 10 I is to be furnished by

the assessee from any Registered Doctor.

Section 80 TTA: Deduction from gross total income in respect of any Income by way of Interest on Savings account

Deduction from gross total income of

an individual or HUF, upto a maximum of Rs. 10,000/-, in respect of

interest on deposits in savings account ( not time deposits ) with a

bank, co-operative society or post office, is allowable (Assessment

Year 2016-17).

Section 80U: Deduction limit has raised in respect of Person suffering from Physical Disability

Deduction

of Rs.75,000/- to an individual who suffers from a physical

disability(including blindness) or mental retardation. Further, if the

individual is a person with severe disability, deduction of Rs.

125,000/- shall be available u/s 80U. Certificate should be obtained

from a Govt. Doctor. The relevant rule is Rule 11D.

Monday, 29 June 2015

Download All in One TDS on Salary for Govt and Non-Govt Employees for the Financial Year 2015-16 and Assessment Year 2016-17 [ This Excel utility can prepare at a time your Tax Compute Sheet + Salary Structure for Govt and Non-Govt Employees Salary Pattern + Automatic HRA Calculation + Automatic Arrears Relief Calculation with Form 10E + Automated Form 16 Part A&B and Part B ]

Tax planning has

always been the test of efficiency for people along with being a test of they can save their taxes in a lawful manner. Here are

some of the tips that can help you to plan your taxes for the F.Y. 2015-16

& A.Y. 2016-17. As per the New Finance Budget 2015-16, In this Budget the

Tax Slab is same as previous Financial Year 2014-15

1) Various Investment in :- U/s 80C

Policies are a prominent way to save a handful amount of tax. Up

to Rs. 1, 50, 000 (A.Y.2016-17) can be saved by way of investing PPF, EPF, Fixed Deposit

for 5 years, Pension Plans, etc. as specified u/s 80C, 80CCC and 80CCD.

2) Contribute to NPS U/s 80CC :- Under Chapter VIA

NPS stands for New

Pension Scheme was has recently been initiated by the Government under which

investors can claim a deduction as a have a Tax free NPS return, however,

withdrawal under such system is till taxable. Max Rs. 1.5 Lakh

3) The aid of Medical Insurance:- U/s 80D

A deduction of Rs. 25,

000 is available for people who wish to invest in medical insurance for self.

This deduction increases to Rs. 30, 000 when it is done by senior citizens.

4) Expenditure towards disabled dependent :- U/s 80DDB

When certain amount is

spent in form medical insurance for a disabled dependent, deduction up to Rs.

80, 000 is available where the disablement is normal in nature.

5) Repayment of Higher Education Loan Interest :- U/s 80E

When repayment is

carried out for higher education loan, the same is also allowed as a deduction

and hence can reduce ample amount of tax liability. Max Rs.1 Lakh

6) Donate :- U/s 80G

Donation to charitable

trusts and organizations have always been regarded as an auspicious event,

therefore, 50% or 100% deduction is available in such context.

7) House

Building

People who are liable to

pay house loan interest can also claim deduction upto Rs. 2 Lakh U/s 24B and

Rs. 1.5 Lakh U/s 80C as HBL Principal amount and Rs. 1 Lakh more can be availed

U/s 80EE w.e.f. 01/04/2013

8) Transportation / Conveyance allowance :- U/s 10

A sum of Rs 19200/- P.A.

can be claimed as a deduction for transportation and conveyance, additionally, and

the Phy. Disable person can get the benefits up to Rs. 38,400/- P.A.

Download All in One TDS on Salary for Govt and Non-Govt Employees for the Financial Year 2015-16 and Assessment Year 2016-17

Thursday, 28 May 2015

Download All in One TDS on Salary for Govt and Non-Govt Employees for the Financial Year 2015-16 and Assessment Year 2016-17 [ This Excel utility can prepare at a time your Tax Compute Sheet + Salary Structure for Govt and Non-Govt Employees Salary Pattern + Automatic HRA Calculation + Automatic Arrears Relief Calculation with Form 10E + Automated Form 16 Part A&B and Part B ]

Tax planning has

always been the test of efficiency for people along with being a test of they can save their taxes in a lawful manner. Here are

some of the tips that can help you to plan your taxes for the F.Y. 2015-16

& A.Y. 2016-17. As per the New Finance Budget 2015-16, In this Budget the

Tax Slab is same as previous Financial Year 2014-15

1) Various Investment in :- U/s 80C

Policies are a prominent way to save a handful amount of tax. Up

to Rs. 1, 50, 000 (A.Y.2016-17) can be saved by way of investing PPF, EPF, Fixed Deposit

for 5 years, Pension Plans, etc. as specified u/s 80C, 80CCC and 80CCD.

2) Contribute to NPS U/s 80CC :- Under Chapter VIA

NPS stands for New

Pension Scheme was has recently been initiated by the Government under which

investors can claim a deduction as a have a Tax free NPS return, however,

withdrawal under such system is till taxable. Max Rs. 1.5 Lakh

3) The aid of Medical Insurance:- U/s 80D

A deduction of Rs. 25,

000 is available for people who wish to invest in medical insurance for self.

This deduction increases to Rs. 30, 000 when it is done by senior citizens.

4) Expenditure towards disabled dependent :- U/s 80DDB

When certain amount is

spent in form medical insurance for a disabled dependent, deduction up to Rs.

80, 000 is available where the disablement is normal in nature.

5) Repayment of Higher Education Loan Interest :- U/s 80E

When repayment is

carried out for higher education loan, the same is also allowed as a deduction

and hence can reduce ample amount of tax liability. Max Rs.1 Lakh

6) Donate :- U/s 80G

Donation to charitable

trusts and organizations have always been regarded as an auspicious event,

therefore, 50% or 100% deduction is available in such context.

7) House

Building

People who are liable to

pay house loan interest can also claim deduction upto Rs. 2 Lakh U/s 24B and

Rs. 1.5 Lakh U/s 80C as HBL Principal amount and Rs. 1 Lakh more can be availed

U/s 80EE w.e.f. 01/04/2013

8) Transportation / Conveyance allowance :- U/s 10

A sum of Rs 19200/- P.A.

can be claimed as a deduction for transportation and conveyance, additionally, and

the Phy. Disable person can get the benefits up to Rs. 38,400/- P.A.

Thursday, 18 December 2014

As per the Central Budget 2014-15, the Income Tax Slab has raised from 2 Lakh to 2.5 Lakh and the Section 80C also hike up to Rs. 1.5 Lakh. The Section 87A as Tax Rebate Rs.2000/- and Savings Bank Interest U/s 80TTA Max Rs. 10,000/- also continue in this financial year.

As per the latest Finance Budget the Tax Liability may reduce to the all salaried persons and get extra benefits from the Tax Section.

Below given Excel Based Software which can prepare at a time your Income Tax Calculation + Automatic House Rent Exemption Calculation + Arrears Relief Calculation with Form 10E + Automated Form 16 Part A&B and Form 16 Part B for all State employees for the Financial Year 2014-15.The Salary Structure build as per the All State Employees Salary Patter, and you can easily calculate your Gross Salary by this Salary Structure.

Click here to Download the All in One TDS on Salary for All State Employees For FY 2014-15

Snapshot of State employees Salary Structure

Wednesday, 3 December 2014

All in One Income Taxpreparation Excel Based Software for West Bengal Govt employees For Ass Yr2015-16( This Excel Utility can prepare at a time your Tax Compute Sheet + Individual Salary Structure + Individual Salary Sheet + Automated HRA Calculation + Form 16 Part A&B and Part B)

Snapshot of Main Data Input Sheet

Snapshot of Salary Structure of W.B.Govt employees

Snapshot of Salary Sheet

Snapshot of Form 16 Part B

Snapshot of Form 16 Part A&B

The Financial Year have already started since the 1/4/2014 and which will be end of March 2015. In this Financial year have already passed the New Central Finance Bill and some Income Tax Section introduce to the Income Tax Payers ( All Salaried Persons). It is observed that the Income Tax Slab has changed up to Rs. 2.5 Lakh and the Section 80C also Raised up to Rs. 1.5 Lakh in this Financial Year 2014-15, Tax Slab For Men and Women is Rs. 2,50,000/- = NIL and 2,00,001 to 10,00,000/- Tax @ 10% and above 10,00,000/- @ 20%.

The New Income Tax Section started from the Financial Year 2013-14 is given below:-

Section 87A Tax Rebate Rs. 2,000/- who's Taxable Income not more than 5,00,000/-

Section 80EE, House Building Loan Interest who's HBL interest started since 1/4/2013 Max Rs. 1,00,000/- additional amount of U/s 24 B.

Download the utility from below link.

Tuesday, 2 December 2014

Click here to download Income Tax Preparation Excel Based Software for the Central Govt employees Financial Year 2014-15 [ This Excel utility can prepare at a time Tax compute sheet + Arrears Relief Calculation with Form 10E + Automated HRA Calculation + Form 16 Part A&B and Form 16 Part B] for the Financial Year 2014-15

Everybody knows that section 80C along with section 80CCC and section 80CCD of Income Tax Act, 1961, allows a tax deduction of Rs 1.5 lakh from the gross total income. Various tax saving options and investment avenues eligible for deductions under section 80C and also discussed the various limitations of section 80C.But, did you know that apart from section 80C, there are many more tax deductions available under section (u/s) 80? You can avail deduction under section 80D for health insurance,

section 80DD & section 80DDB for medical treatment,

section 80E for educational loan,

80G for donations and 80GG for rent paid.

Here’s a list of 7 such deductions available to individuals under section 80:

Medical Based Deductions under Section 80

1. Health insurance premium under section 80D

You can claim a deduction of Rs 15,000 (RS 20,000 in case of senior citizens) under section (u/s) 80D for medical or health insurance--popularly known as mediclaim policy--premiam paid on the health of yourself, spouse and dependent children.

Additionally, (from 1st April, 2008) you’re also allowed a further deduction of Rs 15,000 u/s 80D for buying health insurance policy for your parents (Rs 20,000 if either of your parents is a senior citizen) irrespective of whether they’re dependent on you or not.

Thus, if neither you nor your parents are senior citizens, you’re allowed a maximum deduction of Rs 30,000. On the other hand, if both you and your parents are senior citizens, then the maximum limit allowed under section 80D increases to Rs 40,000.

Please also note that part payment of premium is also eligible for deduction u/s 80D. For example, suppose that your parents buy a health insurance policy having an annual premium of Rs 14,000. Out of the total premium, let’s say your parents pay only Rs 5,000 and the balance of Rs 9,000 is paid by you. So, you’ll be allowed a tax deduction of Rs 9,000 under section 80D and your parents will be allowed a deduction of Rs 5,000.

2. Medical treatment of disabled dependent under section 80DD

You’re also allowed a fixed deduction of Rs 50,000 (irrespective of the actual expenses) u/s 80DD, if you happen to incur any expenditure on the medical treatment (including nursing, training & rehabilitation) of handicapped dependent (spouse, children, parents, brothers and sisters). For severe disability, the amount of deduction available is Rs 75,000.

Here’s a list of 7 such deductions available to individuals under section 80:

Medical Based Deductions under Section 80

1. Health insurance premium under section 80D

You can claim a deduction of Rs 15,000 (RS 20,000 in case of senior citizens) under section (u/s) 80D for medical or health insurance--popularly known as mediclaim policy--premiam paid on the health of yourself, spouse and dependent children.

Additionally, (from 1st April, 2008) you’re also allowed a further deduction of Rs 15,000 u/s 80D for buying health insurance policy for your parents (Rs 20,000 if either of your parents is a senior citizen) irrespective of whether they’re dependent on you or not.

Thus, if neither you nor your parents are senior citizens, you’re allowed a maximum deduction of Rs 30,000. On the other hand, if both you and your parents are senior citizens, then the maximum limit allowed under section 80D increases to Rs 40,000.

Please also note that part payment of premium is also eligible for deduction u/s 80D. For example, suppose that your parents buy a health insurance policy having an annual premium of Rs 14,000. Out of the total premium, let’s say your parents pay only Rs 5,000 and the balance of Rs 9,000 is paid by you. So, you’ll be allowed a tax deduction of Rs 9,000 under section 80D and your parents will be allowed a deduction of Rs 5,000.

2. Medical treatment of disabled dependent under section 80DD

You’re also allowed a fixed deduction of Rs 50,000 (irrespective of the actual expenses) u/s 80DD, if you happen to incur any expenditure on the medical treatment (including nursing, training & rehabilitation) of handicapped dependent (spouse, children, parents, brothers and sisters). For severe disability, the amount of deduction available is Rs 75,000.

Furthermore,

section 80DD also allows deduction on insurance premium paid on certain

specified life insurance policies.

JEEVAN ADHAR policy of Life Insurance

Corporation (LIC) qualifies for deduction under section 80DD.

The policy is

meant for the maintenance of handicapped dependent after the death of the

insured. This is a whole life policy with no maturity value. On the death of

the insured (individual depositing the money), 20% is paid in lump sum and

balance is utilized to pay annuity to the handicapped dependant or the nominee

for the benefit of the handicapped dependent. If the handicapped dependent dies

before the insured, the amount is refunded back and is taxable in the year of

receipt.

There is yet another policy of LIC (JEEVAN VISHWAS) meant for the purpose of providing for the handicapped dependents; however, it is not eligible for deduction section 80DD of the IT Act. It is a with-profit endowment plan with guaranteed and loyalty additions.

There is yet another policy of LIC (JEEVAN VISHWAS) meant for the purpose of providing for the handicapped dependents; however, it is not eligible for deduction section 80DD of the IT Act. It is a with-profit endowment plan with guaranteed and loyalty additions.

The point worth remembering is that section 80DD

allows fixed deduction of Rs 50,000 / Rs 75,000 irrespective of the expenditure

incurred on the medical treatment of the handicapped dependent or amount deposited

in the Jeevan Adhar Policy. It might seem absurd, but it’s true.

To know the specific ailments covered and other

formalities to be completed for availing deduction u/s 80DD.

3. Medical treatment of certain

specified ailments under section 80DDB

You’re also allowed a deduction of actual expenditure incurred—minus any amount reimbursed by employer or by an insurance company—up to Rs 40,000 (Rs 60,000 for senior citizens) for medical treatment of certain specified diseases and ailments (e.g. AIDS, cancer, Parkinson’s disease etc.) of yourself or any dependent family member (spouse, children, parents, bothers and sisters) under section 80DDB subject to certain conditions.

You’re also allowed a deduction of actual expenditure incurred—minus any amount reimbursed by employer or by an insurance company—up to Rs 40,000 (Rs 60,000 for senior citizens) for medical treatment of certain specified diseases and ailments (e.g. AIDS, cancer, Parkinson’s disease etc.) of yourself or any dependent family member (spouse, children, parents, bothers and sisters) under section 80DDB subject to certain conditions.

4. Handicapped person under section 80U

You’re allowed a fixed deduction of Rs 50,000, if you’re suffering from any of the disabilities specified such as blindness, hearing impairment, mental retardation or illness, leprosy-cured, low vision and locomotive disability, autism and celebral palsy. For severe disability, deduction is Rs 75,000. Please note the following points for claiming deduction u/s 80U:

1.

The disability pertains to you (i.e., the taxpayer) and not any of your family

members.

2. You need not spend any amount on the medical treatment.

3. A certificate is required from specified medical authority.

4. For up to 40% disability, nothing is allowed; for disability ranging from 40% to less than 80% a deduction of Rs 50,000 is allowed and if the disability is 80% or more, Rs 75,000 is allowed to be deducted from your gross total income.

2. You need not spend any amount on the medical treatment.

3. A certificate is required from specified medical authority.

4. For up to 40% disability, nothing is allowed; for disability ranging from 40% to less than 80% a deduction of Rs 50,000 is allowed and if the disability is 80% or more, Rs 75,000 is allowed to be deducted from your gross total income.

Other Deductions under Section 80

5. Educational Loan under section 80E

You’re allowed a deduction u/s 80E for the repayment of loan taken (from any bank, financial institution, or approved charitable institution) for higher studies (full time studies including graduation of specified courses such as management, engineering and medicine) for yourself or any of your family members (children, spouse).

However, the deduction u/s 80E is only for the interest portion and unlike home loans, deduction for principal repayment is not allowed. Finally, deduction u/s 80E is limited to a maximum period of 8 years. .

6. Donations under section 80G

Donations paid to specified institutions also qualify for tax deduction under section 80G but is subject to certain ceiling limits. Based on limits, we can broadly divide all eligible donations under section 80G into four categories:

a) 100% deduction without any qualifying limit (e.g., Prime

Minister’s National Relief Fund).

b) 50% deduction without any qualifying limit (e.g., Indira Gandhi Memorial Trust).

c) 100% deduction subject to qualifying limit (e.g., an approved institution for promoting family planning).

d) 50% deduction subject to qualifying limit (e.g., an approved institution for charitable purpose other than promoting family planning).

b) 50% deduction without any qualifying limit (e.g., Indira Gandhi Memorial Trust).

c) 100% deduction subject to qualifying limit (e.g., an approved institution for promoting family planning).

d) 50% deduction subject to qualifying limit (e.g., an approved institution for charitable purpose other than promoting family planning).

The qualifying limit u/s 80G is 10% of the adjusted gross total income.

7. Rent paid under section 80GG

If you’re either self-employed or employed but not getting any HRA from your employer, you can get a deduction under section 80GG for the rent paid by you. However, unlike HRA exemption under section 10(13A) of I.T.Act, here the maximum amount allowed is only Rs 2,000 per month (Rs 24.000 annually) and is also subject to certain conditions.

So, make sure that (in addition to section 80C, 80CCC and 80CCD), you consider all the above tax concessions available to you u/s 80 while doing your tax planning.

In fact, the first course of action while doing your tax planning is to avail to all the tax breaks related to expenses (whether under section 80C or any other section such as 80E) before making any further investment commitments for tax savings under section 80.

Subscribe to:

Posts (Atom)