Most of us are already well aware of the deduction available under section 80C of the Income-tax Act, 1961. The maximum amount of deduction that can be claimed under section 80C is Rs 150000 for FY2016-17 which is the same as for FY2015-16. The section offers various investment options to the taxpayer which not only generate returns for him but can also be claimed as deduction while calculating total taxable income.

|

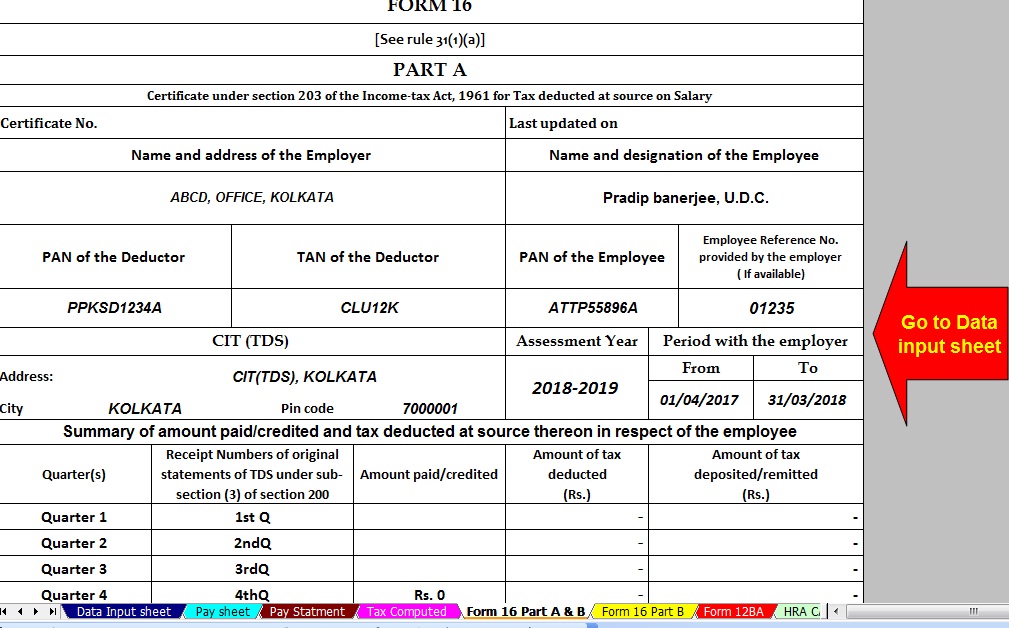

| Details of Employee & Employer's Sheet |

The majority of people invest in life insurance policies, PPF, ELSS etc. in order to avail this deduction, but there are several other options too which are worth considering. Deduction under Section 80C is not only available for investments but also for specified expenditures made by the taxpayer. However, in order to claim the deduction for a particular financial year you need to invest/spend the deductible amount in that financial year.

Here's a list of different investments and expenditures which can be claimed as deduction by the taxpayer under Section 80C for the current financial year i.e. FY16-17

Provident Fund (PF) & Voluntary Provident Fund (VPF)

A part of your salary is deducted monthly as your contribution towards PF. The total amount deducted annually can be claimed by you as deduction while computing your total (taxable) income. An employee can increase this contribution if he is willing to get a less take-home salary. This additional contribution is called VPF and is also eligible for deduction under Section 80C.

So if you don't want to get into the dilemma of choosing and buying the most appropriate investment option to avail tax benefits, then you can simply increase your VPF so that the EPF and VPF contributions total up to Rs 150000.

Public Provident Fund (PPF)

PPF is a scheme provided by the government and the investment in it is eligible for deduction under Section 80C. You can invest as low as Rs 500 and as high as Rs 150000 in a financial year. The interest on PPF is currently tax-free (compounded yearly) and the normal maturity period is 15 years. A point worth noting is that the interest rate is assured but not fixed. The rate is subject to revision every quarter.

Life Insurance Premiums

Any amount that you pay towards life insurance premium for yourself, your spouse or your children can also be included in Section 80C deduction. Please note that the premium paid by you for your parents (father/ mother/ both) or your in-laws is not eligible for deduction under Section 80C. If you are paying the premium for more than one insurance policy, all the premiums can be included. It is not necessary to have the insurance policy from Life Insurance Policy.

Equity Linked Savings Scheme (ELSS)

There are some mutual fund (MF) schemes specially created to offer you tax savings and these are called Equity Linked Savings Scheme (ELSS). The investments that you make in ELSS are eligible for deduction under Section 80C. This is one of the best ways to grow your money and enjoy tax benefit simultaneously as the return generated by ELSS is much more than those generated by other investment products.

Home Loan Principal Repayment

The Equated Monthly Installment (EMI) that you pay to repay your home loan consists of two components - Principal and Interest. The principal qualifies for deduction under Section 80C. Even the interest can save you significant income tax, but that would be under Section 24 and section 80EE of the Income Tax Act.

So if you have an outstanding home loan in your name, then the repayment of the principal amount made by you in a financial year can be claimed as the deduction under Section 80C and you need not invest in other products specifically to avail tax benefits.

National Savings Certificate (NSC)

NSC is a tax-saving instrument with a maturity period of five years. A person can purchase an NSC for as low as Rs 100. Any investments in NSC are eligible for deduction under Section 80C. This interest is compounded half yearly and is taxable.

Five-year Post Office Time Deposit (POTD) Scheme

POTDs are similar to bank fixed deposits. They are available for different time durations like one, two, three and five years but only five-year POT qualifies for tax saving under section 80C. The interest rates offered by them is compounded quarterly but paid annually. Please note that the interest earned is entirely taxable.

Unit linked Insurance Plan (Ulip)

An insurance product which covers life insurance and also provides the benefits of equity investments, Ulips have attracted the attention of investors and tax-savers because of their multiple advantages -life cover, tax-saving and also helping you grow your money by giving decent returns in the long-term.

Payment of Tuition Fees

Paying your kids' school fees is an expenditure which can't be ignored. Now imagine that the amount paid by you as tuition fees (excluding development fee of donation amount), whether at the time of admission or thereafter, is eligible as deduction to you and will help you save tax

Contributions to National Pension System (NPS)

Any contribution made by an individual (whether employed or not) to the National Pension Scheme is also allowed as the deduction to the individual under section 80CCD. Also, note that the combined deduction under section 80C and 80CCD cannot exceed Rs 1.5 lakh. However, if one contributes an additional Rs 50,000 to NPS (over and above the combined limit of Rs 1.5 lakh) it can be claimed as deduction under section 80CCD(1B) i.e. total deduction that can be claimed for contributions to NPS is Rs 1.5 lakh plus Rs 50,000 under two different sections of the Income Tax Act.