Showing posts with label Automatic Income Tax Form 16 Part B for F.Y.2016-17. Show all posts

Showing posts with label Automatic Income Tax Form 16 Part B for F.Y.2016-17. Show all posts

Thursday, 6 July 2017

Wednesday, 5 July 2017

Tuesday, 4 July 2017

Friday, 30 June 2017

Tax Deductions available under section 80 of Income Tax Act, 1961

Section 80C (Individual & HUF) : - In all, total deductions under section 80C, 80CCC and 80CCD (1) cannot exceed Rs 1.50 lakh for the current assessment year. Which means total investments, expenses, and payments up to a limit of Rs 1.50 lakh are eligible for tax deductions mentioned in the above-mentioned sections. These sections cover many savings schemes like National savings certificates (NSCs), Public Provident Fund (PPF) and other pension plans, life insurance premiums, government bond investments. Here’s a section-wise breakup of deductions and exemptions available under the above-mentioned codes:

Section 80CCC (Individual): - This section provides tax deductions for any investments made in an annuity plan or Life Insurance Corporation (LIC) or pension received under funds mentioned in Section 10(23AAB).

Section 80CCD (1) (Individual): - The deductions under this section are aimed at encouraging people to save. These deductions are allowed to people who avail the National Pensions savings scheme (NPS). Under this, an individual can avail a deduction of up to 10 percent of his/her salary or Rs 1.50 lakh whichever is lower if the person has employed or the lower of Rs 1.50 lakhs or 10 percent of gross income, if the individual is self-employed.

Download Automated Master of Form 16 Part B which can prepare at a time 100 Employees Form 16 Part B for F.Y.2016-17

Download Automated Master of Form 16 Part B which can prepare at a time 50 Employees Form 16 Part B for F.Y.2016-17

Section 80CCD (2) (Individual): - This is applicable in the case of employer’s contribution. The maximum deduction of 10% of salary.

Section 80CCD (1B) (Individual): -For the financial year 2015-16 or assessment year 2016-17, this new section provides for an additional tax deduction for the amount contributed to NPS of up to Rs 50,000. So for AY2016-17, total deductions under Section 80 are available up to Rs 200,000.

Section 80D (Individual & HUF): - Deduction up to Rs.25,000 for self, spouse, and dependent children and separate deduction of Rs.30,000 for parents is allowed for the premium paid towards medical insurance.

Section 80DD (Individual & HUF): -Deduction of expenses incurred on medical treatment of Dependent Relative is fixed at Rs.75,000 for 40% disability and Rs.1,25,000 for severe i.e. 80% disability. Claimant is required to furnish a certificate of disability from prescribed authority.

Section 80DDB (Individual & HUF): -Deduction in respect of specified disease for self or dependent relatives is allowed lower of Rs.60,000 or the actual amount paid. This deduction amount increases to Rs.80,000 in the case of the senior citizen.

Section 80E (Individual): -Deduction is also available on interest outgo on education loan for higher studies. This loan could be taken by the assessee, spouse or children or a student for whom the assessee is a legal guardian.

Section 80G (All Assessee): -Donations given to various specified institutions and organizations are allowed to be deducted from your income. The deductions are segregated into two categories i.e. 100% or 50% but cash donations exceeding Rs.10,000 is not allowed to claim.

Section 80GG (Individual): - A deduction on house rent paid is available to those who are not paid house rent allowance (HRA) by the employer. An individual, spouse or minor children shouldn’t own a home at the place of employment of the assessee to claim this deduction. Neither the assessee should have a self-occupied residence at any other place. The deduction available is limited to rent minus 10% of total income or 25% of total income or Rs 2000 (whichever is lower).

Section 80TTA (Individual & HUF): - Any interest earned (up to Rs 10,000) on your deposits in a savings bank account, co-operative society or post office is tax deductible. This excludes fixed deposit interest income.

Section 80U (Individual & HUF) : - Physically Disabled persons can claim deductions under 80U of Rs.1,00,000. The assessee is required to obtain a certificate from Government Doctor.

Section 87A (Individual & HUF) :- Tax Rebate Rs. 5,000/- from the Financial Year 2016-17

Thursday, 22 June 2017

In this fast moving world, young individuals switch job more often with an aim to get a better opportunity and better increment.

Form 16, is very vital for the salaried employee while filing tax returns.

However, a situation may arise when they have to file returns and are left with multiple Form 16. Here are 10 things you must know on Form 16.

Download and prepare at a time 50 employees Automated Master of Form16 Part B for F.Y.2016-17 & A.Y.2017-18

Download and prepare at a time 100 employees Automated Master of Form16 Part B for F.Y.2016-17 & A.Y.2017-18

1) Form 16 is issued by the employer to employee. This certificate provides all details of salary earned and tax deducted at source by the employer.

2) If a person has changed job, he needs to collect the Form 16 from both the employer at the year end, with the help of both forms only he would able to file his returns.

3) An individual can have multiple Form 16 in cases such as a change in job or work with multiple employers simultaneously.

4) If your salary drawn is below the basic exemption limit, you may not be issued with this certificate by your employer as no TDS is deducted.

5) If your employer has not provided with Form 16, you can check the salary slip as it will mention the same.

6) Form 16 includes key information required such as gross salary, perquisites, various allowances, and deductibles.

7) If you have changed the job in the same financial year, authorities require you, to sum up, the total income from both the employers and file income tax return.

8) If the previous employer has not issued form 16 on account of some reason such as no tax deduction at its end, the employee can file the return taking into consideration the pay-slips plus the form 16 issued by the new employer.

9) If you do not wish to furnish form 16 issued by your previous employer to the new employer, you can file tax return taking cues from the two form 16 issued by the previous and new employer.

10) Form 16 will must mention the PAN Number of the employer.

Wednesday, 21 June 2017

Income Tax Deductions are allowed by the Income Tax Act as an instrument for tax saving and reducing the liability to pay tax. The act provides a list of deductions.

Indian Income Tax Act, 1961 provides various income tax deductions. The income tax deductions can be reduced from the gross taxable income while filing the income tax return. These deductions help in tax saving and reducing the tax liability of a person. The income tax is imposed on the total income as per the income tax slab rates after claiming the income tax deductions.

The list of the income tax deductions is as under.

Download Automatic 50 employees Master of Form 16 Part B for F.Y.2016-17 & A.Y.2017-18 [ This Excel Based Software can prepare at a time 50 employees Form 16 Part B for F.Y.2016-17]

Section 80C: Deduction, u/s 80C, is the most ordinary income tax deduction available for individuals and HUFs. One can claim deduction under this part by making an investment in some specified instruments like Provident Funds, National Saving Certificates, Life Insurance Policy, Mutual Funds, etc. The maximum limit for claiming deduction under Section 80C is Rs. 150000.

Section 80CCC: This deduction is available to Individuals for contributing to certain pension funds. The deduction is allowed for the amount paid as premium for annuity plan of any insurance company. The limit for this deduction is Rs. 150000 maximum.

Section 80CCD: The deduction is available for individuals contributing to the pension scheme of Central Government, i.e., depositing in a notified pension scheme. The limit u/s 80CCD for a salaried person is 10% of his salary. In other cases, the contribution is restricted to 10% of the total gross income.

Note: The maximum limit of Rs. 150000 is a cumulative limit for section 80C and section 80CCC for every Financial Year. Additionally, an amount of Rs. 50000 is allowed as a deduction over and above this limit of Rs. 150000, if invested in National Pension Scheme. Hence, it can be concluded that the maximum limit for the above three sections cumulatively is Rs. 200000.

Download Automated Master of Form 16 Part A&B which can prepare at a time 50 employees Form 16 Part A&B for Financial Year 2016-17 & Assessment Year 2017-18

Section 80CCG: A resident individual being a retail investor can claim a deduction for investments made in notified equity savings scheme. The total gross income of the individual must be less than or equal to Rs. 12 lakhs for availing this exemption. The deduction is limited to lower of 50% of the amount invested in the scheme or Rs. 25000. The assessee can claim a deduction for three years consecutively starting with the assessment year in which acquisition took place.

Section 80DD: Any resident individual or HUF can claim a deduction for an amount spent on the medical treatment of a disabled dependent. It also includes rehabilitation expenses or amounts contributed in any scheme made for this. The person can claim a flat deduction of Rs. 75000. However, a person with a disability of 80% or more can claim a deduction of Rs. 125000.

Download Automated Master of Form 16 Part B with 12 BA which can prepare at a time 50 employees Form 16 Part B with 12 BA for Financial Year 2016-17 and assessment Year 2017-18

Section 80D: Any individual or HUF is eligible for deduction u/s 80D for contributing toward medical health insurance and health check-up. The deduction can be claimed for himself along with spouse, children (dependent). A maximum of Rs. 25000 or Rs. 30000 (if an individual or its spouse is a senior citizen) can be claimed as a deduction.

Section 80DDB: Any amount contributed towards medical treatment of specified diseases by an individual or HUF is allowed as a deduction under this section. Individual also include dependent spouse, children, siblings or parents. The maximum amount is lower of the actual sum paid or Rs. 40000 minus the reimbursement of the insurance company. In the case of senior citizen the limit of Rs. 40000 is replaced by Rs. 60000 whereas, for super senior citizen it is amended by replacing Rs. 80000.

Download Automated Income Tax Form 16 Part B for F.Y.2016-17 & A.Y.2017-18 which can prepare at a time 100 employees Form 16 Part B for Financial Year 2016-17

Section 80E: The interest on the loan is taken for higher education of an individual or its spouse or children, by the person from financial institutions is allowed for deduction. The deduction can be claimed for interest payment starting from the year of interest payment commencement and seven years immediately following it or until the full interest is paid, whichever is earlier.

Section 80G: All the assesses donating an amount in certain specified funds or charitable institutions or whatever named called, can claim deduction under this section. Firstly, qualifying amount is calculated and based on that category of deduction is identified. However, if any sum paid in cash is more than Rs. 10000, then no deduction is allowed.

Section 80GG: The individuals who don't receive house rent allowance can claim the deduction for the rent paid, amount being least of the following:

· 25% of the total income;

· Rent paid minus 10% of the total income;

· Rs. 5000 per month.

No deduction is allowed if any residential accommodation is owned by the city of work by the individual or his spouse or minor child or his HUF.

Download Automatic 50 employees Master of Form 16 Part A&B for Financial Year 2016-17 & Assessment Year 2017-18, which can prepare at time 50 employees Form 16 Part A&B

Section 80TTA: Any individual or HUF receiving interest on the savings account deposits can claim a deduction for the amount received subject to a maximum of Rs. 10000. Interest earned on time deposits is excluded.

Section 80U: A resident individual is allowed a deduction if he is certified as disabling by the medical authority. A flat deduction of Rs. 75000 or Rs. 125000 (80% or more disability) can be claimed.

Tax Rebate U/s 87A: The Tax Rebate can be allowed up to Rs. 2500/- who’s taxable income less than 3.5 Lakh.

Monday, 22 May 2017

The CBDT completely changed the Format of Form 16 and there have in two parts One is Part A and another One is Part B. This Format of Form 16 have changed vide Notification dated on 19/2/2013. In Form 16 Part A have the all details of tax deducted and and credited in to the Central Govt and another Form 16 Part B where the Employee's Salary details. In this Form 16 Part B there have not any column to where you can put the employees Name or Pan Number. Look the below Snap Shot of Form 16 Part B:-

This Form 16 Part B must be prepare by the Employer where the found details of Salary of Employee.

If you prepare the Form 16 Part B then where you can mention the employees Identity like as Name of Employee and Pan Card Number. It is most hazard to identify to who's Form 16 Part B is prepared ?

But the Form 16 Part A where have only the Tax Deducted and Deposited in to the Central Govt The Form 16 part A is Mandatory to Download from the TRACES Portal (www.tdscpc.gov.in)

The Snap Shot of Form 16 Part A is given below,Look the Snap Shot of Form 16 Part A:-

Feature of those Utility:-

- Automatic Calculate the Income Tax

- Automatic Prepare the Form 16 Part B

- Automatic Prepare the Form 16 Part A&B and Part B

- Automatic prepare 50 employees Form 16 Part B ( prepare at a time 50 employees Form 16)

- Prevent the Double entry of PAN and Name of Employee

- Automatic Convert the Amount in to the In Words

- Easy to Install in any computer

- Easy to Generate in any Version 2003 OR 2007 OR 2010

Download the utility from below:-

1) Download One by One preparation Form 16 PartA&B and Part B for F.Y.2016-17

2) Download One by One Form 16 Part B for F.Y.2016-17

3) Download Master of Form 16 Part A&B for 50 employees

4) Download Master of 50 employees Form 16 Part B for F.Y.2016-17

5) Download Master of Form 16 Part B with 12 BAfor F.Y. 2016-17

Tuesday, 21 February 2017

With some tinkering in the income tax rates for 2017-18, Finance Minister Arun Jaitley reduced the tax rate for income between Rs. 2.5 lakh and Rs. 5 lakh to 5 per cent in the Union Budget, while adding a surcharge of 10 per cent on tax for income between Rs. 50 lakh and Rs. 1 crore.

Although the basic income tax exemption limit remains the same at Rs. 2.5 lakh, there are many exemptions available in the Income Tax Act, which can substantially reduce your tax liability.

One needs to plan from the beginning of the next financial year to take maximum benefit of the income tax deductions available.

Here are the some of the deductions available for FY2017-18:

House Rent Allowance under Section 10 (13A) of the Income Tax Act

House Rent Allowance, commonly known as HRA, makes up a major chunk of a salaried individual’s total pay. HRA is partly exempted from tax. If you are staying in your own house or not paying any rent, your HRA will be completely taxable. However, those who stay with their parents can also claim HRA benefits by paying rent to their parents.

The amount which is allowed for exemption under HRA is calculated as the minimum of:

1) Rent paid annually minus 10 per cent of basic salary plus dearness allowance

2) Actual HRA received

3) 40 per cent of basic and dearness allowance (50 per cent in case of metro cities)

Download Automated Income Tax Form 16 Part B for Financial Year 2016-17& Ass Year 2017-18 [ This Excel Utility can prepare at a time 100 employeesForm 16 Part B ]

Deductions under Section 80C

Section 80C of the Income Tax Act provides various provisions under which an individual can get deduction benefits up to Rs. 1.5 lakh. Employees’ Provident Fund (EPF), Public Provident Fund (PPF), Sukanya Samriddhi Account, National Savings Certificate and tax-saving fixed deposits are some of the investment options that offer benefits under Section 80C. The premium paid for life insurance plans, National Pension Scheme (NPS) and tax-saving mutual funds (ELSS) also qualify for deduction under Section 80C.

Further, one can claim tuition fees paid for up to two children, principal repayment on the home loan, stamp duty and registration cost on the house bought as the deduction under Section 80C.

Deductions under Section 80CCD(1B)

Introduced in Budget 2015-16, Section 80CCD (1B) provides deduction up to Rs. 50,000 for investment in NPS Tier 1 account. This deduction is over and above the deduction available in Section 80C. An individual in 30 percent tax bracket can save up to Rs. 15,450 of tax by investing Rs. 50,000 in NPS.

Deduction of interest on housing loan (Section 24B)

Buying a house is among several other things an individual wants to do during his or her lifetime. The income tax rules also incentivise the same. Under Section 24B of the Income Tax Act, interest paid up to Rs. 2 lakh on housing loan and up to Rs. 30,000 on home improvement loan is allowable as the deduction from your taxable income.

The government has however cut down tax benefits borrowers enjoyed on properties let out on rent. As per current tax laws, for properties rented out, a borrower could deduct the entire interest paid on home loan after adjusting for the rental income. On the other hand, borrowers of self-occupied properties get Rs. 2 lakh deduction on interest repayment on a home loan.

However, according to the proposed change in Budget 2017, on rented properties, the borrower can only claim the deduction of up to Rs. 2 lakh per year after adjusting for the rental income. And the amount of Rs. 2 lakh can be carried forward for eight assessment years.

Since the interest component of home loan repaid in initial years is higher, experts say that the borrower may not be able to fully adjust the interest paid as the deduction even in subsequent years.

Deduction under Section 80EE

Under Section 80EE, an additional deduction of Rs. 50,000 is available over and above the limit of Section 24B on interest paid on home loans if the person is buying a house for the first time (the person must not own any other residential property on the date of sanction of a loan). However, to avail the benefit of this section the value of the property must be below Rs. 50 lakh and the loan amount should not exceed Rs. 35 lakh. Further, the property must be bought after April 1, 2016.

Deduction under Section 80D

Premium paid for medical/health insurance for self, spouse, children, and parents qualify for deduction under this Section. On can claim the deduction of Rs. 25,000, if he is below 60 years of age, and Rs. 30,000 if he is above 60 years of age, towards medical insurance premium paid for self, spouse, and children. Further, an additional deduction of Rs. 25,000 is available if one has bought medical insurance for his parents. This deduction can go up to Rs. 30,000 if parents are above the age of 60 years.

Deduction under Section 80DD

If a tax payer has dependent parents, spouse, children or siblings who are differently-abled, then he can claim deductions up to Rs. 75,000 for expenses on their maintenance and medical treatment under this section. This deduction can increase to Rs. 1.25 lakh in case of severe disability.

Deduction under Section 80DDB

Under this section, one can claim the deduction of Rs. 40,000 for a treatment of certain diseases for self and dependents. The deduction can go up to Rs. 60,000 if the tax payer is above 60 years of age and if he is above 80 years of age, then the deduction amount is up to Rs. 80,000.

Deduction under Section 80E

According to the provisions of Section 80E, a taxpayer can claim the deduction for interest paid on education loan for him, spouse or children. There is no upper limit on the amount of deduction. However, the loan must have been taken from a financial institutional or approved charitable institution and for full-time higher education.

Tax Rebate U/s 87A :- Max Rs. 2500/- from the F.Y.2017-18 & A.Y.2018-19

Deduction U/s 87A : - Exemption Savings Bank Interest Max Rs. 10,000/-

Sunday, 22 January 2017

This time is preparing your Income Tax Papers and Income Tax statement as per the Finance Budget 2016-17. Your Employer asks to you submit the Income Tax Statement within March 2016. If you not prepared the Income Tax Statement with your all deposit and yet not submit the same to your Employer, then the Employer can deduct your Income Tax as per your Total Earn without any deduction U/s 80C or Under Chapter VIA.

Below given a Excel Based Income Tax preparation Software which can prepare at a time your Individual Salary Sheet + Individual Tax Compute sheet + Individual Salary Structure + Automatic House Rent Exemption Calculation U/s 10(13A) + Automatic Arrears Relief Calculation with Form 10E + Automated Form 16 Part A&B and Form 16 Part B for F.Y.2016-17. Just put your salary details into the Salary Structure and all the Income Tax papers will be prepared automatically.

The feature of this Excel Utility:-

1) This Excel Utility can easy to generate just like as an Excel File

2) This Excel Utility can use both of Govt and Non-Govt Employees ( Private Employee)

3) Automatic H.R.A. Exemption Calculation can be done

4) Automatic Arrears Relief Calculation with Form 10E up to the F.Y.2016-17

5) Automatic Convert the Amount into the In-Words

6) All the Tax Section Amended version have in this utility.

Click here to Download the All in One TDS on Salary for Govt and Non-Govt Employees for F.Y.2016-17

|

| Employee's & Employer Data Sheet |

|

| Deduction Sheet Section wise |

|

| Tax Compute Sheet |

|

| Arrears Relief Main Data Input Sheet |

| |

| Arrears Relief Form 10E |

Monday, 9 January 2017

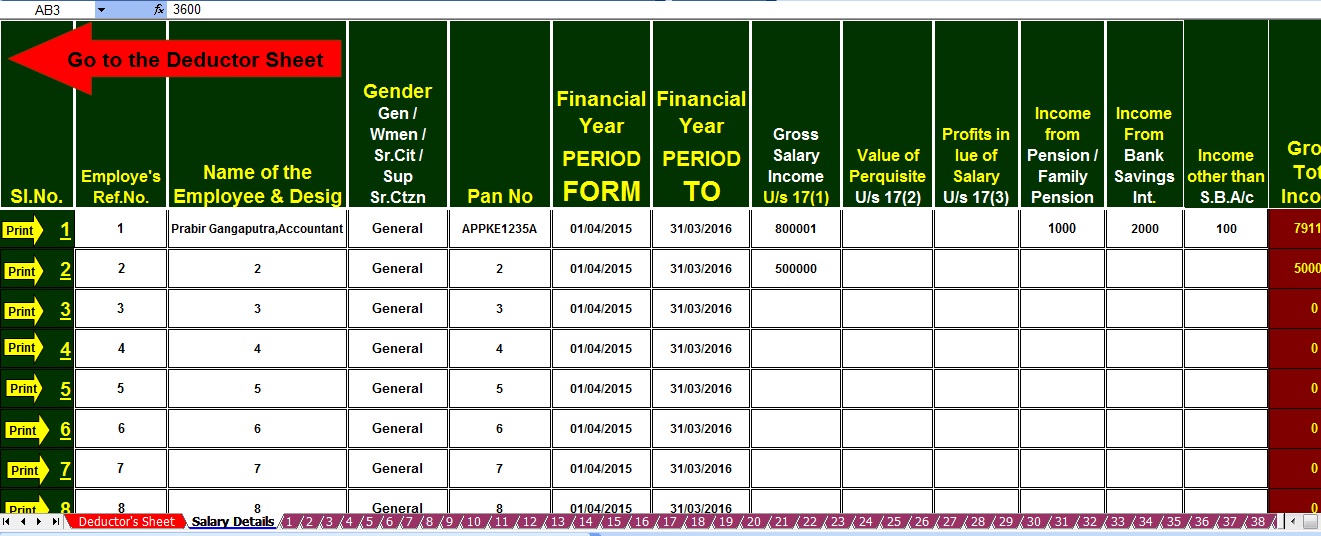

Download Automatic Master of Form 16 Part B for the Financial Year 2016-17 and Assessment Year 2017-18. This Excel Based software can prepare at a time 50 employees Form 16 Part B.

Feature of this Excel Utility:-

1) Prepare at a time 50 employees Form 16 Part B for F.Y.2016-17

2) All the Income Tax amended tax section with the enhance tax limit as per Finance Bill 2016-17

3)This Excel Utility can use both of Government and Private Concerned

4) This Excel utility can easy to install in any computer

5) You can prepare more than 500 employees Form 16 Part B ( First prepare 50 then prepare 50 etc)

6) Automatic Tax calculate

7) Automatic Convert the Amount in to the In-Word without any Excel Formula.

Click here to Download Automatic Income Tax Form 16 Part B for F.Y.2016-17

|

| Deductor's Details Sheet |

|

| Tax deduction Salary Sheet Section Wise |

| |

| Income Tax Form 16 |

Tuesday, 20 December 2016

The income tax slab of 2016 -17 is same as earlier. However, the middle class will get the tax benefit of Rs 3000. Almost 1 crore people will enjoy this tax benefit. The budget 2016 did not change the income tax slab. The tax relief is given through the rebate.

There is few more opportunity to save tax. The first time home buyer would get extra tax saving on the home loan interest. Those who lives in the rented house, also have a reason to cheer.

The budget 2016 has also fulfilled the long time demand of Tax exemption on NPS withdrawal. This demand has been partially met. The companies which employ the fresher would get some financial benefit due to the new EPF rules. The TDS rules of EPF is also relaxed.

While there are many tax benefits to the middle class and employees, the rich has to bear more tax burden. I will discuss all these new tax decisions. Along with this, you would also learn the new income tax slab rate of 2016. You would also learn the tax calculation as well. [toc]

Budget 2016 – Main Points Related to Tax

No Change in Income Tax Slab

The income tax slab for individuals, females, senior citizen remains same in the FY 2016-17. There is no change. The basic exemption remains at 2.5 lacs. There is no extra concession for females.

Income Tax Rebate Increased

The income tax rebate is increased by Rs 3000. In the FY 2015-16, it was Rs 2000, now the tax rebate is Rs 5000. This rebate is available to those whose taxable income is below 5 lacs. It means, that the tax liability of such people would come down by Rs 5000. Because of this provision, those who earns up to Rs 3 lacs are not required to pay any tax. Rather, if a person uses the all available deductions, the income up to Rs 5 lacs can become tax-free.

Download from below link the Automatic Income Tax Form 16 Part B for F.Y.2016-17 [ This Excel Utility can prepare at a time 50 employees and 100 employees Form 16 Part B ]

1) Click here to Download Master of Form 16 Part B for 50 employees for F.Y.2016-17

2) Click here to Download Master of Form 16 Part B for 100 employees for F.Y.2016-17

Rent Deduction Increased

The tax deduction for the rent payment (section 80GG) is increased from 24,000 to 60,000. This deduction is available to those who lives in rented house and do not get House Rent Allowance from the employer.

More Deduction On Home Loan Interest

The home buyer would have the opportunity to claim more tax deduction. The budget 2016 has increased the tax deduction for home loan interest by 50 thousand. This extra deduction of 50,000 would be available over and above the 80C limit of Rs 1.5 lac. It means, your total tax deduction under section 80C can go up to Rs 2 lacs provided you are paying at least 50,000 as home loan interest. This extra tax deduction is available to those homebuyers who buy a home in the financial year 2016 – 2017. The cost of the house should be more than 50 lacs and home loan amount should not be more than 35 lacs.

In FY 2014-15, The government has given similar tax benefit on the home loan interest.

Surcharge Rate Increased For Individuals

The income tax surcharge is levied on the taxpayers who earns more than Rs one crore in a year. For individuals, this surcharge was 12%. But budget 2016 has increased the burden of surcharge for them. Now the surcharge on income tax has become 15%. The surcharge for all other categories of the taxpayers would remain same.

The Income Tax Slab For FY 2016-17 and AY 2017-18

Now I am giving you the tax slab and rates of the financial year 2016-17. These tax rates are applicable on the income earned during 1 April 2016-31 march 2017. You should take account of this income tax slab rate. The assessment of income tax according to this slab rate will be done in the year 2017-18. It means you have to apply these rates while filing the income tax return in 2017.

Besides the income tax rates, the surcharge is also charged if total taxable income exceeds Rs 1 Crore. Since the budget 2016, the income tax surcharge on individuals is increased to 15%. Two years back it was mere 10%. However, marginal relief is given in such cases.

Income Tax Slab for

2016 – 17

|

Tax Rate

|

Below 2.5 Lakh

|

NIL

|

2.5 Lakh to 5 Lakh

|

10% of the amount above and over 2,50,000.

|

5 Lakh to 10 Lakh

|

Rs. 25,000 + 20% of the amount by which the taxable income exceeds Rs. 5,00,000

|

Above 10 Lakh

|

Rs. 1,25,000 + 30% of the amount by which the taxable income exceeds Rs. 10,00,000

|

Subscribe to:

Posts (Atom)