1. The tax rate for income between Rs 2.5 lakh to Rs 5 lakhs has been reduced to 5% from 10%

Showing posts with label Sec 24B. Show all posts

Showing posts with label Sec 24B. Show all posts

Friday, 4 August 2017

Monday, 26 September 2016

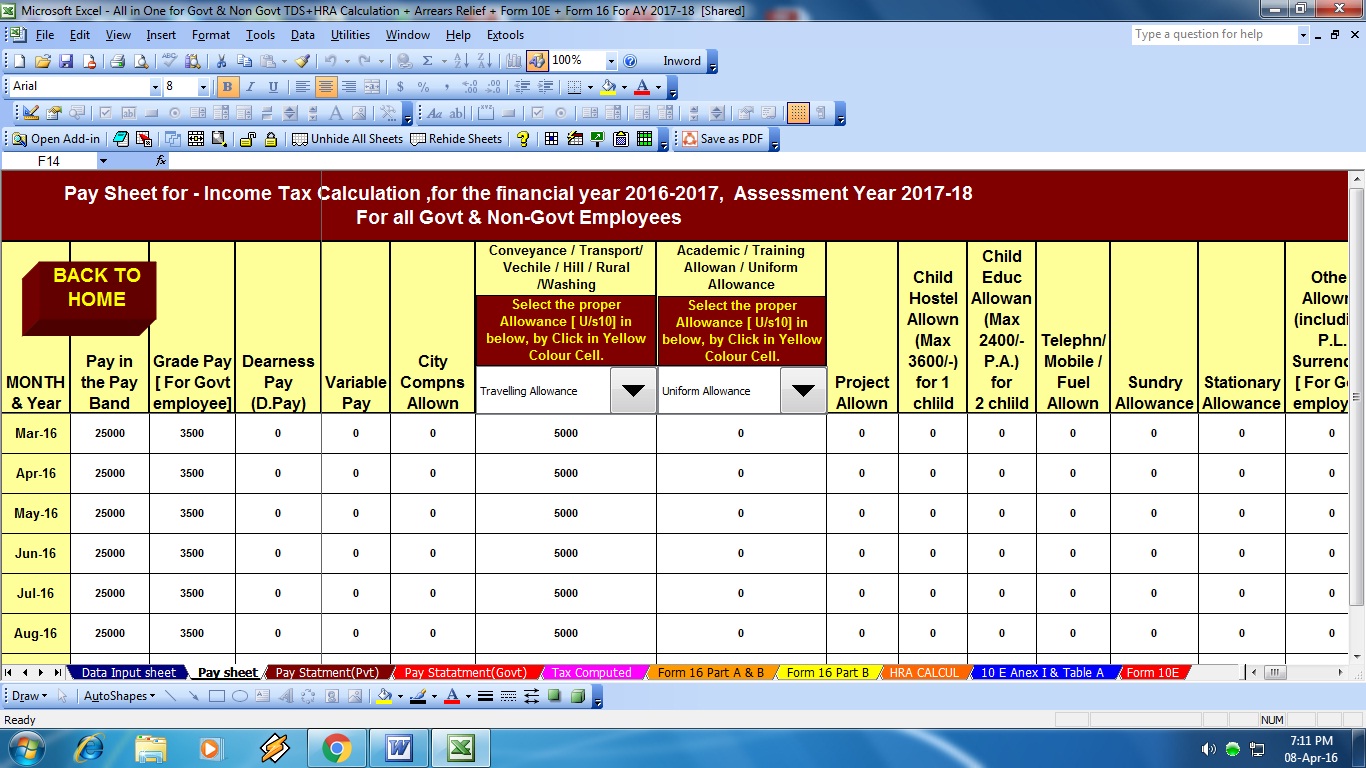

Download All in One Income Tax Preparation Excel Based Software for Bihar State Govt employees for F.Y.2016-17 [ This Utility can prepare at a time Individual Tax Compute Sheet + Automatic H.R.A.Exemption Calculation + Automatic Form 16 Part A&B and Form 16 Part B for F.Y.2016-17]

Section 24 & 80EE of the income tax act provides deduction in respect of home loan interest.

Important points U/s 24B & U/s 80EE

1) Interest on housing loan is allowable as the deduction on accrual basis not on paid basis (even if account books are kept on the cash basis) if capital is borrowed for the purpose of purchase, construction, repair, renewal or reconstruction of the house property. The deduction can be claimed for two or more housing loans.

2)Interest includes service fees, brokerage, commission, prepayment charges etc.

3)Interest/penalty on unpaid interest shall not be allowed as deduction.

4)The deduction shall be allowed irrespective of the nature of loan whether it is housing loan or personal loan from any person/institution.

5) If a person instead of raising a loan from a third party pays sale price to the seller in installments along with interest than such interest is also allowable.

6) Interest on borrowed money which is payable outside India shall not be allowed as deduction under section 24(b), unless the tax on the same has been paid or deducted at source and in respect of which there is no person in India, who may be treated as an agent of the recipient for such purpose.

7) For claiming deduction under this section, the assessee must be the owner or deemed owner of the house property and loan shall be in the assessee name.

Maximum Limit of deduction under section 24B

These limits of deduction are applicable assessee wise and not property wise. Therefore if an assessee owns two or more house property then the total deduction for that assessee remain same.

1) In Let Out Property/Deemed to be Let Out – No maximum limit

2) Self Occupied House (SOP) – Rs. 2,00,000. (1,50,000 for A.y 2014-15 and before)

In the following cases, the above limit of Rs 2,00,000 for SOP shall be reduced to Rs. 30,000

– Loan borrowed before 01-04-1999 for any purpose related to house property.

– Loan borrowed after 01-04-1999 for any purpose other than construction or acquisition.

– If construction/acquisition is not completed within 5 years from the end of the financial year (3 years till the financial year 2015-16) in which capital was borrowed. For example, a loan is obtained for construction/acquisition on 28 Oct 2011 then the deduction limit should reduce to Rs 30,000 if the construction/acquisition completes after 31 March 2017.

Also Extra Deduction of Rs. 1,50,000 on Home Loan Interest under Section 80EE w.e.f. 1/4/2016

Interest for pre-construction/acquisition period

Interest for pre-construction/acquisition period is allowable in 5 equal installments beginning from the year of completion of house property. This deduction is not allowable if the loan is utilized for repairs, renewal or reconstruction.

Pre-Construction/Acquisition period starts from the date of borrowing and ends on the last day of preceding Financial Year in which the construction is completed. For example, if house property is completed on 21st March 2012 then the deduction is allowed from Financial Year 2011-2012 to 2015-16.

Deduction in case of Co-borrower

If the home loan is taken on joint names then the deduction is allowed to each co-borrower in proportion to his share in the loan. For taking such deduction it is necessary that such co-borrower must also be co-owner of that property. If the assessee is a co-owner but is repaying the full loan himself, then he can claim the deduction of full interest paid by him.

The limit of deduction in case of Self occupied property applies individually to each co-borrower . In other words, each co-borrower can claim deduction up to Rs. 2 lakh/Rs. 30,000. No limit is applicable to let out property.

Interest Deduction with HRA

HRA under section 10(13A) and interest deduction can be availed simultaneously even if house property is in the same city in which you resides on rented property.

Form 12BB is to be filed with employer if you want your employer to take deduction under this section into consideration and thus deduct lower TDS

Monday, 4 July 2016

Changes in Income Tax Rules as per the Finance Budget 2016-17 & A.Y.2017-18:

1. There has been no change in the income tax slabs for the Financial Year 2016-17 & Assessment Year 2017-18.

2. For people with net taxable income below Rs 5 lakh, the tax rebate has been increased from Rs 2,000 to Rs 5,000 u/s 87A. This would benefit people who have net taxable income between Rs 2.7 Lakhs to Rs 5 Lakhs.

3. Additional exemption for first time home buyer up to Rs. 50,000 on interest paid on housing loans. This would be applicable where the property cost is below Rs 50 Lakhs and the home loan is below Rs 35 lakhs. The loan should be sanctioned on or after April 1, 2016.

4. Tax Exemption u/s 80GG (for rent expenses who do have HRA component in salary) has been increased from Rs 24,000 to Rs 60,000 per annum. This is a good move to align the exemption amount with today’s rent and keep the section relevant.

5. For people with net taxable income above Rs 1 crore, the surcharge has been increased from 12% to 15%

6. Dividend Income in excess of Rs. 10 lakh per annum to be taxed at 10%

7. 40% of lump sum withdrawal on NPS at maturity would be exempted from Tax. This rule now also applies to EPF. So now in the case of EPF income tax would be applicable on 60% of the corpus in maturity.

8. Presumptive taxation scheme introduced for professionals with receipts up to Rs. 50 lakhs. The presumptive income would be 50% of the revenues.

Download All in One TDS on Salary for Govt & Non-Govt employees for F.Y.2016-17 & A.Y.2017-18 [This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure + Automated Arrears Relief Calculation with Form 10E up to F.Y.2016-17 + Automatic H.R.A. Exemption Calculation + Automated Form 16 Part A&B + Automated Form 16 Part B ]

1. Section 80C/80CCC/80CCD

1. Section 80C/80CCC/80CCD

Download All in One TDS on Salary for Govt & Non-Govt employees for F.Y.2016-17 & A.Y.2017-18 [This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure + Automated Arrears Relief Calculation with Form 10E up to F.Y.2016-17 + Automatic H.R.A. Exemption Calculation + Automated Form 16 Part A&B + Automated Form 16 Part B ]

1. Section 80C/80CCC/80CCD

These 3 are the most popular sections for tax saving and have a lot of options to save tax. The maximum exemption combining all the above sections is Rs 1.5 lakhs. 80CCC deals with the pension products while 80CCD includes Central Government Employee Pension Scheme.

You can choose from the following for tax saving investments:

1. Employee/ Voluntary Provident Fund (EPF/VPF)

2. PPF (Public Provident fund)

3. Sukanya Samriddhi Account

4. National Saving Certificate (NSC)

5. Senior Citizen’s Saving Scheme (SCSS)

6. 5 years Tax Saving Fixed Deposit in banks/post offices

7. Life Insurance Premium

8. Pension Plans from Life Insurance or Mutual Funds

9. NPS (New Pension Scheme)

10. Equity Linked Saving Scheme (ELSS – popularly known as Tax Saving Mutual Funds)

11. Central Government Employee Pension Scheme

12. Principal Payment on Home Loan

13. Stamp Duty and registration of the House

14. Tuition Fee for 2 children

2. Section 80CCD(1B) – Investment in NPS

Budget 2015 has allowed additional exemption of Rs 50,000 for investment in NPS. We have done a complete analysis and concluded that it would be beneficial for you to discard this benefit and invest after-tax money in a good equity mutual fund.

Download All in One TDS on Salary for Central Govt Employees for F.Y.2016-17 & A.Y.2017-18 [This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure as per Central Govt Salary Patterns + Automatic H.R.A. Exemption Calculation + Automated Form 16 Part A&B + Automated Form 16 Part B ]

3. Payment of interest on Home Loan (Section 24/80EE)

3. Payment of interest on Home Loan (Section 24/80EE)

The interest paid up to Rs 2 lakhs on home loan for the self-occupied home is exempted u/s 24. There is no limit for home given on rent.

Budget 2016 has provided additional exemption up to Rs 50,000 for payment of home loan interest for first time home buyers. To avail this benefit the value of the home should not exceed Rs 50 lakhs and loan should not be more than Rs 35 lakhs.

4. Payment of Interest on Education Loan (Section 80E)

The total interest paid on education loan can be claimed as tax exemption. There is no upper limit for the same.

5. Investment in RGESS (Section 80CCG)

Deduction Up to Rs 25,000 (50% of the amount invested) is allowed if you make the investment in preapproved stocks and mutual funds in Rajiv Gandhi Equity Savings Scheme (RGESS). This is available to first-time equity investors subject to certain conditions.

6. Medical insurance for Self and Parents (Section 80D)

You can get the tax deduction up to Rs 60,000 by paying the medical insurance premium for self, your dependents, and your parents. There is also sub-limit of Rs 5,000 for the preventive medical checkup.

7. Treatment of Serious disease (Section 80DDB)

You can claim deduction up to Rs 80,000 for treatment of certain diseases like AIDS, renal failure, etc for self or dependents

8. Physically Disabled Tax-payer (Section 80U)

Physically Disabled Tax-payer can get tax exemption up to Rs 1.25 lakhs u/s 80U

9. Physically Disabled Dependent (Section 80DD)

You can claim deduction up to Rs 1.25 lakhs for maintenance and medical treatment of Physically Disabled dependent

10. Donations to Charitable Institutions (Section 80G)

Deduction up to Rs 40,000 is allowed for Donation to certain charitable funds, charitable institutions, etc.

11. Donations to Charitable Institutions (Section 80GGA)

Deduction up to Rs 1 lakh is allowed for donations for scientific research or rural development

12. Donations to Charitable Institutions (Section 80GGC)

Deduction up to Rs 60,000 is allowed for donations to political parties

Download All in One TDS on Salary for Only Non-Govt employees for F.Y.2016-17 & A.Y.2017-18 [This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure as per Non-Govt Salary Patterns + Automatic H.R.A. Exemption Calculation + Automated Form 12 BA + Automated Form 16 Part A&B + Automated Form 16 Part B ]

Along with the tax saving options, it also has details about all the common salary components and their tax treatment. This section can help you to plan your salary components in case your company offers such facility.

We hope that this eBook would help you in understanding, planning and saving taxes.

Wednesday, 29 June 2016

Changes in Income Tax Rules as per the Finance Budget 2016-17 & A.Y.2017-18:

1. There has been no change in the income tax slabs for the Financial Year 2016-17 & Assessment Year 2017-18.

2. For people with net taxable income below Rs 5 lakh, the tax rebate has been increased from Rs 2,000 to Rs 5,000 u/s 87A. This would benefit people who have net taxable income between Rs 2.7 Lakhs to Rs 5 Lakhs.

3. Additional exemption for first time home buyer up to Rs. 50,000 on interest paid on housing loans. This would be applicable where the property cost is below Rs 50 Lakhs and the home loan is below Rs 35 lakhs. The loan should be sanctioned on or after April 1, 2016.

4. Tax Exemption u/s 80GG (for rent expenses who do have HRA component in salary) has been increased from Rs 24,000 to Rs 60,000 per annum. This is a good move to align the exemption amount with today’s rent and keep the section relevant.

5. For people with net taxable income above Rs 1 crore, the surcharge has been increased from 12% to 15%

6. Dividend Income in excess of Rs. 10 lakh per annum to be taxed at 10%

7. 40% of lump sum withdrawal on NPS at maturity would be exempted from Tax. This rule now also applies to EPF. So now in the case of EPF income tax would be applicable on 60% of the corpus in maturity.

8. Presumptive taxation scheme introduced for professionals with receipts up to Rs. 50 lakhs. The presumptive income would be 50% of the revenues.

Download All in One TDS on Salary for Govt & Non-Govt employees for F.Y.2016-17 & A.Y.2017-18 [This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure + Automated Arrears Relief Calculation with Form 10E up to F.Y.2016-17 + Automatic H.R.A. Exemption Calculation + Automated Form 16 Part A&B + Automated Form 16 Part B ]

1. Section 80C/80CCC/80CCD

1. Section 80C/80CCC/80CCD

These 3 are the most popular sections for tax saving and have a lot of options to save tax. The maximum exemption combining all the above sections is Rs 1.5 lakhs. 80CCC deals with the pension products while 80CCD includes Central Government Employee Pension Scheme.

You can choose from the following for tax saving investments:

1. Employee/ Voluntary Provident Fund (EPF/VPF)

2. PPF (Public Provident fund)

3. Sukanya Samriddhi Account

4. National Saving Certificate (NSC)

5. Senior Citizen’s Saving Scheme (SCSS)

6. 5 years Tax Saving Fixed Deposit in banks/post offices

7. Life Insurance Premium

8. Pension Plans from Life Insurance or Mutual Funds

9. NPS (New Pension Scheme)

10. Equity Linked Saving Scheme (ELSS – popularly known as Tax Saving Mutual Funds)

11. Central Government Employee Pension Scheme

12. Principal Payment on Home Loan

13. Stamp Duty and registration of the House

14. Tuition Fee for 2 children

2. Section 80CCD(1B) – Investment in NPS

Budget 2015 has allowed additional exemption of Rs 50,000 for investment in NPS. We have done a complete analysis and concluded that it would be beneficial for you to discard this benefit and invest after-tax money in a good equity mutual fund.

Download All in One TDS on Salary for Central Govt Employees for F.Y.2016-17 & A.Y.2017-18 [This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure as per Central Govt Salary Patterns + Automatic H.R.A. Exemption Calculation + Automated Form 16 Part A&B + Automated Form 16 Part B ]

Download All in One TDS on Salary for Central Govt Employees for F.Y.2016-17 & A.Y.2017-18 [This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure as per Central Govt Salary Patterns + Automatic H.R.A. Exemption Calculation + Automated Form 16 Part A&B + Automated Form 16 Part B ]

3. Payment of interest on Home Loan (Section 24/80EE)

The interest paid up to Rs 2 lakhs on home loan for the self-occupied home is exempted u/s 24. There is no limit for home given on rent.

Budget 2016 has provided additional exemption up to Rs 50,000 for payment of home loan interest for first time home buyers. To avail this benefit the value of the home should not exceed Rs 50 lakhs and loan should not be more than Rs 35 lakhs.

4. Payment of Interest on Education Loan (Section 80E)

The total interest paid on education loan can be claimed as tax exemption. There is no upper limit for the same.

5. Investment in RGESS (Section 80CCG)

Deduction Up to Rs 25,000 (50% of the amount invested) is allowed if you make the investment in preapproved stocks and mutual funds in Rajiv Gandhi Equity Savings Scheme (RGESS). This is available to first-time equity investors subject to certain conditions.

6. Medical insurance for Self and Parents (Section 80D)

You can get the tax deduction up to Rs 60,000 by paying the medical insurance premium for self, your dependents, and your parents. There is also sub-limit of Rs 5,000 for the preventive medical checkup.

7. Treatment of Serious disease (Section 80DDB)

You can claim deduction up to Rs 80,000 for treatment of certain diseases like AIDS, renal failure, etc for self or dependents

8. Physically Disabled Tax-payer (Section 80U)

Physically Disabled Tax-payer can get tax exemption up to Rs 1.25 lakhs u/s 80U

9. Physically Disabled Dependent (Section 80DD)

You can claim deduction up to Rs 1.25 lakhs for maintenance and medical treatment of Physically Disabled dependent

10. Donations to Charitable Institutions (Section 80G)

Deduction up to Rs 40,000 is allowed for Donation to certain charitable funds, charitable institutions, etc.

11. Donations to Charitable Institutions (Section 80GGA)

Deduction up to Rs 1 lakh is allowed for donations for scientific research or rural development

12. Donations to Charitable Institutions (Section 80GGC)

Deduction up to Rs 60,000 is allowed for donations to political parties

Download All in One TDS on Salary for Only Non-Govt employees for F.Y.2016-17 & A.Y.2017-18 [This Excel Based Software can prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure as per Non-Govt Salary Patterns + Automatic H.R.A. Exemption Calculation + Automated Form 12 BA + Automated Form 16 Part A&B + Automated Form 16 Part B ]

Along with the tax saving options, it also has details about all the common salary components and their tax treatment. This section can help you to plan your salary components in case your company offers such facility.

We hope that this eBook would help you in understanding, planning and saving taxes.

Subscribe to:

Posts (Atom)